Porsche 2007 Annual Report Download - page 141

Download and view the complete annual report

Please find page 141 of the 2007 Porsche annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

|

|

138

To our shareholders

The Company

The new Panamera

Financials

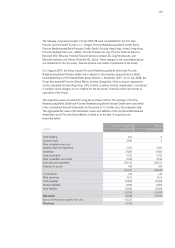

With respect to measurement, IAS 39 distinguishes between the following categories of

financial assets:

– Financial assets at fair value through profit or loss (FVtPL) and held for trading (HfT)

– Held-to-maturity investments (HtM)

– Available-for-sale financial assets (AfS)

– Loans and receivables (LaR).

By contrast, financial liabilities are divided into the two categories:

– Financial liabilities at fair value through profit or loss (FVtPL) and held for trading (HfT) and

– Financial liabilities measured at amortised cost (FLAC).

Depending on the category, measurement of financial instruments is either at fair value or

amortized cost.

Fair value corresponds to market price provided the financial instruments measured are traded

on an active market. If there is no active market for a financial instrument, fair value is calculated

using appropriate actuarial methods such as recognized option price models or discounting future

cash flows with the market interest rate and by confirmations from the banks processing the trans-

actions. Amortized cost corresponds to costs of purchase less redemption, impairment losses

and the reversal of any difference between costs of purchase and the amount repayable upon

maturity in accordance with the effective interest method. Financial instruments are recognized as

soon as Porsche becomes a party to the financial instrument. They are generally derecognized

when the contractual right to cash flow expires or this right is transferred to a third party.

Primary financial instruments

Financial instruments which are recognized at fair value contain securities in the held-for-trading

category and financial assets which are initially recognized as financial assets at fair value through

profit or loss. Gains and losses from subsequent measurement are recognized in the net profit or

loss. Financial instruments classified upon initial recognition at fair value through profit or loss

include hybrid securities, index and discount certificates.

Financial instruments which are held to maturity are accounted for at cost. Gains and losses from

subsequent measurement are recognized in net profit or loss.

Financial instruments categorized as available for sale are measured at fair value. Unrealized

gains and losses from subsequent measurement are recognized in equity after considering

deferred taxes until the investment is disposed of or an objective impairment occurs. Equity

investments disclosed as financial assets and not measured at equity also constitute available-

for-sale investments and are measured at fair value. If no active market exists and fair value

cannot reasonably be expected to be determined, they are measured at cost.

Financial assets are subjected to an impairment test if there is an indication that the value of the

asset may be permanently impaired. An impairment loss is immediately recorded as an expense.

Any loss previously recorded in equity for available-for-sale investments is then also posted to the

income statement. Any increase in value at a later date is accounted for debt instruments by

reversal of the impairment loss through profit or loss.