NVIDIA 2005 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2005 NVIDIA annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

|

|

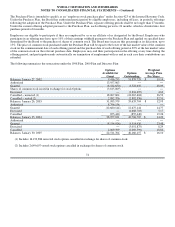

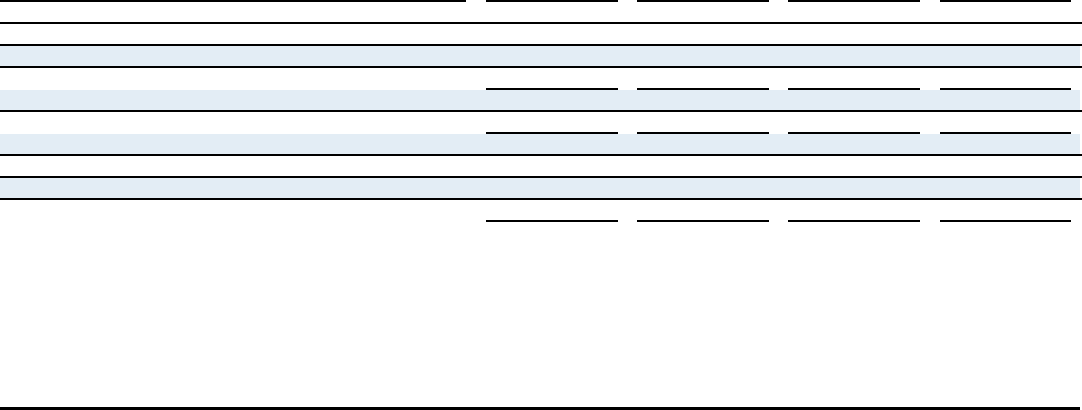

NVIDIA CORPORATION AND SUBSIDIARIES

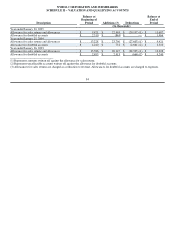

SCHEDULE II − VALUATION AND QUALIFYING ACCOUNTS

Description

Balance at

Beginning of

Period Additions (3) Deductions

Balance at

End of

Period

(In thousands)

Year ended January 30, 2005

Allowance for sales returns and allowances $ 9,421 $ 22,463 $ (20,197) (1) $ 11,687

Allowance for doubtful accounts $ 2,310 $ (844) $ −− $ 1,466

Year ended January 25, 2004

Allowance for sales returns and allowances $ 13,228 $ 23,796 $ (27,603) (1) $ 9,421

Allowance for doubtful accounts $ 4,240 $ 731 $ (2,661) (2) $ 2,310

Year ended January 26, 2003

Allowance for sales returns and allowances $ 15,586 $ 20,147 $ (22,505) (1) $ 13,228

Allowance for doubtful accounts $ 2,493 $ 2,413 $ (666) (2) $ 4,240

______________________________

(1) Represents amounts written off against the allowance for sales returns.

(2) Represents uncollectible accounts written off against the allowance for doubtful accounts.

(3) Allowances for sales returns are charged as a reduction to revenue. Allowances for doubtful accounts are charged to expenses.

84