NVIDIA 2005 Annual Report Download - page 13

Download and view the complete annual report

Please find page 13 of the 2005 NVIDIA annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

|

|

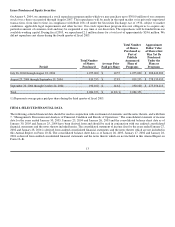

Inventory and Working Capital

Our management focuses considerable attention on managing our inventories and other working−capital−related items. We

manage inventories by communicating with our customers and then using our industry experience to forecast demand on a

product−by−product basis. We then place manufacturing orders for our products that are based on this forecasted demand. The

quantity of products actually purchased by our customers as well as shipment schedules are subject to revisions that reflect changes in

both the customers' requirements and in manufacturing availability. We generally maintain substantial inventories of our products

because the semiconductor industry is characterized by short lead time orders and quick delivery schedules.

Research and Development

We believe that the continued introduction of new and enhanced products designed to deliver leading 3D graphics, high definition

video, audio, ultra−low power communications, storage, and secure networking performance and features is essential to our future

success. Our research and development strategy is to focus on concurrently developing multiple generations of GPUs, MCPs and

WMPs using independent design teams. Our research and development efforts are performed within specialized groups consisting of

software engineering, hardware engineering, very large scale integration, or VLSI, design engineering, process engineering,

architecture and algorithms. These groups act as a pipeline designed to allow the efficient simultaneous development of multiple

generations of products.

A critical component of our product development effort is our partnerships with leaders in the computer aided design, or CAD,

industry. We invest significant resources in the development of relationships with industry leaders, including Cadence Design

Systems, Inc., and Synopsys, Inc., often assisting these companies in the product definition of their new products. We believe that

forming these relationships and utilizing next−generation development tools to design, simulate and verify our products will help us

remain at the forefront of the 3D graphics market and develop products that utilize leading−edge technology on a rapid basis. We

believe this approach assists us in meeting the new design schedules of PC manufacturers.

We have substantially increased our engineering and technical resources from fiscal 2004, and have 1,231 full−time employees

engaged in research and development as of January 30, 2005, compared to 1,057 employees as of January 25, 2004. During fiscal

2005, 2004 and 2003, we incurred research and development expenditures of $335.1 million, $270.0 million and $224.9 million,

respectively.

Competition

The market for GPUs, MCPs and WMPs for PCs, handhelds and consumer electronics is intensely competitive and is characterized by

rapid technological change, evolving industry standards and declining average selling prices. We believe that the principal competitive

factors in this market are performance, breadth of product offerings, access to customers and distribution channels, backward−forward

software support, conformity to industry standard APIs, manufacturing capabilities, price of digital media processors and total system

costs of add−in boards or motherboards. We expect competition to increase both from existing competitors and new market entrants

with products that may be less costly than ours, or may provide better performance or additional features not provided by our

products. In addition, it is possible that new competitors or alliances among competitors could emerge and acquire significant market

share.

We expect substantial competition from Intel's publicized focus on moving to selling platform solutions dominated by Intel products,

such as the Centrino platform. An additional significant source of competition is from companies that provide or intend to provide

GPU, MCP and WMP solutions for the PC, consumer electronics and handheld segments. Our competitors include the following:

•suppliers of MCPs that incorporate a combination of 3D graphics, networking, audio, communications and Input/Output, or

I/O, functionality as part of their existing solutions, such as ATI Technologies, Inc., or ATI, Broadcom Corporation, or

Broadcom, Intel, Silicon Integrated Systems, Inc. and VIA Technologies, Inc., or VIA;

•suppliers of standalone desktop GPUs that incorporate 3D graphics functionality as part of their existing solutions, such as

ATI, Creative Technology, Matrox Electronics Systems Ltd. and XGI Technology, Inc.;

7