NVIDIA 2004 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2004 NVIDIA annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

|

|

August 28, 2001, effected in the form of a 100% stock dividend. The transfer agent distributed the shares resulting from the split on

September 17, 2001. All share and per−share numbers contained herein reflect this stock split.

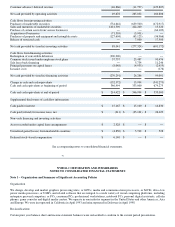

Revenue Recognition

We recognize revenue from product sales when persuasive evidence of an arrangement exists, the product has been delivered, the

price is fixed and determinable and collection is reasonably assured. For all sales, we use a binding purchase order and in certain cases

we use a contractual agreement as evidence of an arrangement. We consider delivery to occur upon shipment provided title and risk of

loss have passed to the customer. At the point of sale, we assess whether the arrangement fee is fixed and determinable and whether

collection is reasonably assured. If we determine that collection of a fee is not reasonably assured, we defer the fee and recognize

revenue at the time collection becomes reasonably assured, which is generally upon receipt of cash.

Our policy on sales to distributors and stocking representatives is to defer recognition of revenue and related cost of revenue until the

distributors and representatives resell the product.

We record estimated reductions to revenue for customer programs at the time revenue is recognized. Our customer programs

primarily involve rebates, which are designed to serve as sales incentives to resellers of our products in various target markets. We

account for rebates in accordance with Emerging Issues Task Force Issue 01−9, or EITF 01−9, Accounting for Consideration Given

by a Vendor to a Customer (Including a Reseller of the Vendor’s Products) and, as such, we accrue for 100% of the potential rebates

and do not apply a breakage factor. Unclaimed rebates, which historically have not been significant, are reversed to revenue upon

expiration of the rebate. Rebates typically expire six months from the date of the original sale.

Our customer programs also include marketing development funds, or MDFs, which we also account for in accordance with EITF

01−9. MDFs represent monies paid to retailers, system builders, OEMs, distributors and add−in card partners that are earmarked for

market segment development and expansion and typically are designed to support our partners’ activities while also promoting

NVIDIA products.

If market conditions decline, we may take actions to increase amounts offered under customer programs, possibly resulting in an

incremental reduction of revenue at the time such programs are offered.

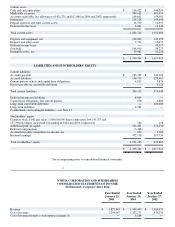

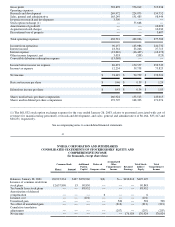

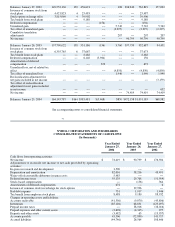

44

NVIDIA CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS – (Continued)

We also record a reduction to revenue by establishing a sales return allowance for estimated product returns at the time revenue is

recognized, based primarily on historical return rates. However, if product returns for a particular fiscal period exceed historical return

rates we may determine that additional sales return allowances are required to properly reflect our estimated exposure for product

returns.

Concentration of Credit Risk

Financial instruments that potentially subject us to concentrations of credit risk consist primarily of cash equivalents, marketable

securities and trade accounts receivable. All marketable securities are held in our name, managed by several investment managers and

held by one major custodial institution. Three customers accounted for approximately 54% of our accounts receivable balance at

January 25, 2004. We perform ongoing credit evaluations of our customers’ financial condition and maintain an allowance for

potential credit losses. This allowance consists of an amount identified for specific customers and an amount based on overall

estimated exposure. Our overall estimated exposure excludes amounts covered by credit insurance and letters of credit.

Impairment of Long−Lived Assets

In accordance with Statement of Financial Accounting Standards No. 144, or SFAS No. 144, Accounting for the Impairment or

Disposal of Long−Lived Assets, long−lived assets, such as property and equipment, and intangible assets subject to amortization, are

reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be

recoverable. Recoverability of assets to be held and used is measured by a comparison of the carrying amount of an asset to estimated

undiscounted future cash flows expected to be generated by the asset. If the carrying amount of an asset exceeds its estimated future

cash flows, an impairment charge is recognized by the amount by which the carrying amount of the asset exceeds the fair value of the

asset. Fair value is determined based on the estimated discounted future cash flows expected to be generated by the asset. Assets to be

disposed of would be separately presented in the consolidated balance sheet and reported at the lower of the carrying amount or fair

value less costs to sell, and would no longer be depreciated. The assets and liabilities of a disposed group classified as held for sale

would be presented separately in the appropriate asset and liability sections of the consolidated balance sheet.

Accounting for Asset Retirement Obligations

In fiscal 2004, we adopted Statement of Financial Accounting Standards No. 143, or SFAS No. 143, Accounting for Asset Retirement