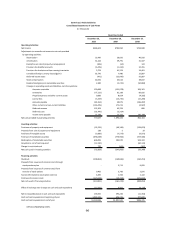

Garmin 2010 Annual Report Download - page 87

Download and view the complete annual report

Please find page 87 of the 2010 Garmin annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

|

|

75

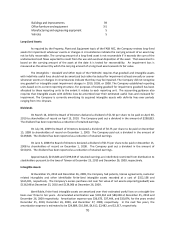

A ajoit of the Copas eseah ad deelopet is pefoed i the Uited States. Reseah ad

development costs, which are expensed as incurred, amounted to approximately $277,261, $238,378, and

$206,109 for the years ended December 25, 2010, December 26, 2009, and December 27, 2008, respectively.

Customer Service and Technical Support

Customer service and technical support costs are included as selling, general and administrative expenses

in the accompanying consolidated statements of operations. Customer service and technical support costs include

costs associated with performing order processing, answering customer inquiries by telephone and through Web

sites, e-mail and other electronic means, and providing free technical support assistance to customers. The

technical support is provided within one year after the associated revenue is recognized. The related cost of

providing this free support is not material.

Software Development Costs

The FASB ASC topic entitled Software requires companies to expense software development costs as they

incur them until technological feasibility has been established, at which time those costs are capitalized until the

product is available for general release to customers. Our capitalized software development costs are not

significant as the time elapsed from working model to release is typically short. As required by the Research and

Development topic of the FASB ASC, costs we incur to enhance our existing products or after the general release of

the service using the product are expensed in the period they are incurred and included in research and

development costs in the accompanying consolidated statements of operations.

Accounting for Stock-Based Compensation

The Company currently sponsors three stock based employee compensation plans. The FASB ASC topic

entitled Compensation – Stock Compensation requires the measurement and recognition of compensation

expenses for all share-based payment awards made to employees and directors including employee stock options

and restricted stock based on estimated fair values. See Note 9.

Accounting guidance requires companies to estimate the fair value of share-based payment awards

on the date of grant using an option-pricing model. The value of the portion of the award that is ultimately

expected to vest is recognized as stock-based compensation expenses over the requisite service period in the

Copas osolidated fiaial stateets.

As stock-based compensation expenses recognized in the accompanying consolidated statement of income

are based on awards ultimately expected to vest, they have been reduced for estimated forfeitures. Accounting

guidance requires forfeitures to be estimated at the time of grant and revised, if necessary, in subsequent periods

if actual forfeitures differ from those estimates. Forfeitures were estimated based on historical experience and

aageets estiates.

Recently Issued Accounting Pronouncements

In January 2010, the FASB issued Accounting Standards Update (ASU) No. 2010-06, "Improving Disclosures

about Fair Value Measurements" ("ASU 2010-06"), which is included in the ASC Topic 820 (Fair Value

Measurements and Disclosures). ASU 2010-06 requires new disclosures on the amount and reason for transfers in

and out of Level 1 and 2 fair value measurements. ASU 2010-06 also requires disclosure of activities, including

purchases, sales, issuances, and settlements within the Level 3 fair value measurements and clarifies existing

disclosure requirements on levels of disaggregation and disclosures about inputs and valuation techniques. Except

as otherwise provided, ASU 2010-06 is effective for interim and annual reporting periods beginning after