Experian 2009 Annual Report Download - page 128

Download and view the complete annual report

Please find page 128 of the 2009 Experian annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

126 Experian Annual Report 2009

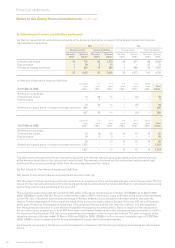

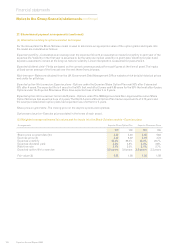

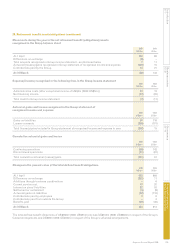

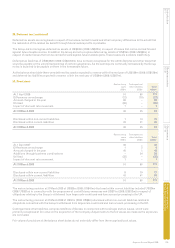

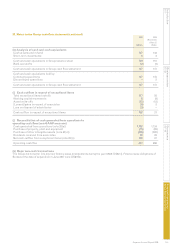

28. Retirement benet assets/obligations (continued)

Changes in the market value of the plans’ assets

2009 2008

US$m US$m

At 1 April 1,045 1,069

Differences on exchange (261) 11

Additions through business combinations – 6

Expected return on plans’ assets 69 76

Actuarial losses on assets (236) (101)

Contributions paid by the Group 14 21

Contributions paid by employees 4 6

Contributions paid from outside the Group – 3

Benets paid (40) (46)

At 31 March 595 1,045

The actual return on plans’ assets was a loss of US$167m (2008: loss of US$25m).

Contributions expected to be paid to the Experian dened benet pension plans during the next nancial year are US$11m by

the Group and US$3m by employees.

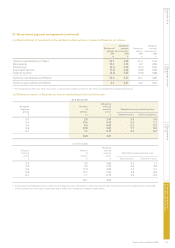

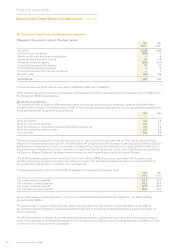

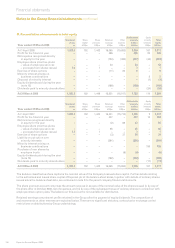

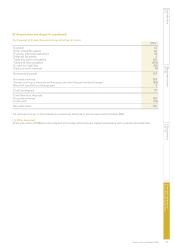

Actuarial assumptions

The valuations used at 31 March 2009 have been based on the most recent actuarial valuations, updated by Watson Wyatt

Limited to take account of the requirements of IAS 19. The principal actuarial assumptions used to calculate the present value

of the dened benet obligations were as follows:

2009 2008

% %

Rate of ination 3.4 3.6

Rate of increase for salaries 5.2 5.4

Rate of increase for pensions in payment and deferred pensions 3.4 3.6

Rate of increase for medical costs 6.5 6.5

Discount rate 6.9 6.9

The main nancial assumption is the real discount rate, i.e. the excess of the discount rate over the rate of ination. If this

assumption increased/decreased by 0.1%, the dened benet obligations would decrease/increase by approximately US$11m

and the annual current service cost would remain unchanged. The discount rate is based on the market yields on high quality

corporate bonds of appropriate currency and term to the dened benet obligations. In the case of the Group’s principal plan,

the Experian Pension Scheme, the obligations are primarily in sterling and have a maturity of some 18 years.

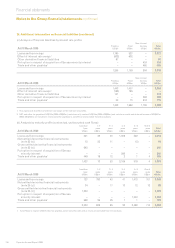

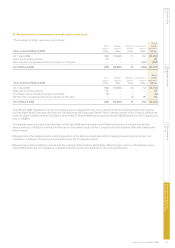

The IAS 19 valuation assumes that mortality will be in line with the PA92 series year of use tables with medium cohort

mortality improvement projections and an age rating of +1 year. This includes an explicit allowance for anticipated future

improvements in life expectancy (medium cohort projections).

The average expectation of life on retirement at age 65 in normal health is assumed to be:

2009 2008

years years

For a male currently aged 65 21.3 21.2

For a female currently aged 65 24.2 24.1

For a male currently aged 50 22.2 22.2

For a female currently aged 50 25.0 25.0

An increase in assumed life expectancy of 0.1 years would increase the dened benet obligations at 31 March 2009 by

approximately US$3m.

The assumptions in respect of discount rate, salary increases and mortality all have a signicant effect on the IAS 19

accounting valuation. Changes to these assumptions in the light of prevailing conditions may have a signicant impact on

future valuations.

The IAS 19 valuation, in respect of post-retirement healthcare benets, additionally assumes a rate of increase for medical

costs. If this assumption increased/decreased by 1.0% per annum the obligation would increase/decrease by US$1m and the

current service cost would remain unchanged.

Notes to the Group nancial statements continued

Financial statements