Dollar Tree 2010 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2010 Dollar Tree annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

Management’s Discussion And Analysis

Of Financial Condition And Results Of Operations

Overview

Our net sales are derived from the sale of merchandise.

Two major factors tend to affect our net sales trends.

First is our success at opening new stores or adding

new stores through acquisitions. Second, sales vary at

our existing stores from one year to the next. We refer

to this change as a change in comparable store net

sales, because we compare only those stores that are

open throughout both of the periods being compared.

We include sales from stores expanded during the year

in the calculation of comparable store net sales, which

has the effect of increasing our comparable store net

sales. The term ‘expanded’ also includes stores that

are relocated.

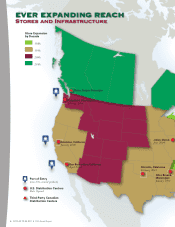

At January 29, 2011, we operated 4,101 stores in

48 states and the District of Columbia, as well as the

Canadian provinces of British Columbia, Ontario,

Alberta and Saskatchewan, with 35.1 million selling

square feet compared to 3,806 stores with 32.3 million

selling square feet at January 30, 2010. During fi scal

2010, we opened 235 stores, expanded 95 stores,

acquired 86 stores and closed 26 stores, compared to

240 new stores opened, 75 stores expanded and 25

stores closed during fi scal 2009. In the current year

we increased our selling square footage by 8.8%.

Of the 2.8 million selling square foot increase in 2010,

0.4 million was added by expanding existing stores

and 0.7 million was added with the acquisition of

Dollar Giant. The average size of our stores opened in

2010 was approximately 8,400 selling square feet (or

about 10,200 gross square feet). For 2011, we continue

to plan to open stores that are approximately 8,000 –

10,000 selling square feet (or about 10,000 –12,000

gross square feet). We believe that this store size is our

optimal size operationally and that this size also gives

our customers an ideal shopping environment that

invites them to shop longer and buy more.

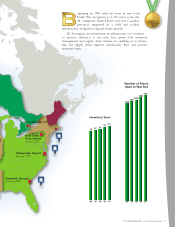

In fi scal 2010, comparable store net sales increased

by 6.3%. The comparable store net sales increase was

primarily the result of a 5.0% increase in the number

of transactions and a 1.3% increase in average ticket.

We believe comparable store net sales continued to be

positively affected by a number of our initiatives, as

debit and credit card penetration continued to increase

in 2010, and we continued the roll-out of frozen

and refrigerated merchandise to more of our stores.

At January 29, 2011, we had frozen and refrigerated

• On May 26, 2010, the Company’s Board of

Directors approved a 3-for-2 stock split in the

form of a 50% common stock dividend. New

shares were distributed on June 24, 2010 to share-

holders of record as of the close of business on

June 10, 2010. As a result, all share and per share

data in this Annual Report have been retroactively

adjusted to refl ect this dividend having the effect

of a 3-for-2 stock split.

• We assign cost to store inventories using the retail

inventory method, determined on a weighted

average cost basis. From our inception and through

fi scal 2009, we used one inventory pool for this

calculation. Because of our investments over the

years in our retail technology systems, we were

able to refi ne our estimate of inventory cost under

the retail method and on January 31, 2010, the fi rst

day of fi scal 2010, we began using approximately

30 inventory pools in our retail inventory calcula-

tion. As a result of this change, we recorded a

non-recurring, non-cash charge to gross profi t and

a corresponding reduction in inventory, at cost, of

$26.3 million in the fi rst quarter of 2010. This was

a prospective change and did not have any effect

on prior periods.

• On November 2, 2009, we purchased a new

distribution center in San Bernardino, California.

We have spent approximately $31.0 million in

capital expenditures for this new distribution

center during fi scal 2009 and an additional $5.7

million in fi scal 2010. This new distribution center

replaced our Salt Lake City, Utah leased facility

whose lease ended in April 2010.

• On February 20, 2008, we entered into a fi ve-

year $550.0 million unsecured Credit Agreement

(the Agreement). The Agreement provides for a

$300.0 million revolving line of credit, including

up to $150.0 million in available letters of credit,

and a $250.0 million term loan. The interest rate

on the facility is based, at our option, on a LIBOR

rate, plus a margin, or an alternate base rate, plus

a margin.

DOLLAR TREE, INC. ♦ 2010 Annual Report 15