Airtran 2008 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2008 Airtran annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

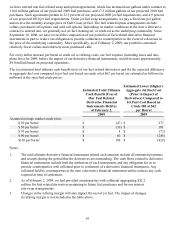

Fuel Related Derivative Financial Instrument Arrangements

We enter into fuel related derivative financial instruments to reduce the ultimate variability of cash flows

associated with fluctuations in jet-fuel prices. The financial accounting for fuel related derivatives is discussed

in ITEM 8. “FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA, Note 4 – Financial Instruments”

and our exposure to market risk is discussed in ITEM 7A. “QUANTITATIVE AND QUALITATIVE

DISCLOSURES ABOUT MARKET RISK – Aviation Fuel .” In summary, our fuel related derivative financial

instruments impacted our 2008 financial statements as follows:

• Net realized gains related to derivative financial instruments that qualify for hedge accounting

reduced fuel expense by $15.7 million during 2008.

• We recorded non-operating net losses related to derivative financial instruments that do not

qualify for hedge accounting of $150.8 million during 2008. During 2008, we realized losses

related to derivative financial instruments that do not qualify for hedge accounting of $126.3

million (including $109 million to unwind certain derivative financial instruments pertaining to

2009 fuel requirements). Realized losses include $41.2 million that settled in cash in early

January 2009.

• As of December 31, 2008, the estimated fair value of our fuel related derivative financial

instruments was a net liability of $65.5 million. The fair value of our fuel related derivatives is in

large part a function of the current market and futures prices of the underlying commodities.

Consequently, changes in the current market and futures prices tend to have a substantial impact

on the fair value of the fuel related derivatives.

• As of December 31, 2008, other accumulated comprehensive income included $7.7 million

(before income tax) of net unrealized losses which had not yet been recognized in the

Consolidated Statements of Operations.

We provide counterparties to our derivative financial instrument arrangements with collateral when the fair

value of our obligation exceeds specified amounts. As of December 31, 2008, we provided counterparties to

fuel and interest rate related derivative financial instruments with collateral aggregating $69.2 million. As of

February 2, 2009, the collateral that we provided counterparties decreased to $32.2 million largely as a result of

the unwinding of certain derivative financial instruments pertaining to 2009 fuel requirements. The collateral is

classified as restricted cash if the funds are held in our name and is classified as deposits held by counterparties

to derivative financial instruments if the funds are held by the counterparty. Any future increases in the fair

value of our obligations under derivative financial instruments may obligate us to provide additional collateral

to counterparties which would reduce our unrestricted cash and investments. Any future decreases in the fair

value of our obligations would result in the release of collateral to us and consequently would increase our

unrestricted cash and investments. Any outstanding collateral is released to us upon settlement of the related

derivative financial instrument liability. Our obligation to provide collateral pursuant to fuel related derivative

financial instrument arrangements tends to be inversely related to fuel prices; consequently, to the extent fuel

prices decrease we will experience lower fuel expense and higher collateral requirements. Because we hedge

significantly less than 100 percent of our fuel requirements, over time a sustained decrease in fuel prices tends

to produce a net cash benefit even though a significant decrease in fuel prices may cause a net use of cash in the

period when prices decrease. Since September 30, 2008, we have revised the composition of our portfolio of

fuel related derivative financial instruments in part to reduce our obligation to provide collateral to

counterparties in the event of a decrease in the price of the underlying commodity. More specifically, as of

February 2, 2009, our portfolio contained relatively fewer collars and relatively more purchased calls.

52