United Healthcare 2010 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2010 United Healthcare annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

|

|

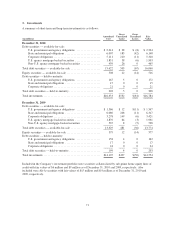

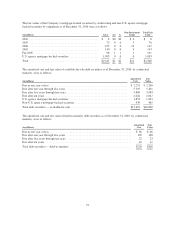

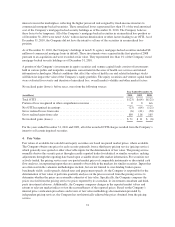

In instances in which the inputs used to measure fair value fall into different levels of the fair value hierarchy, the

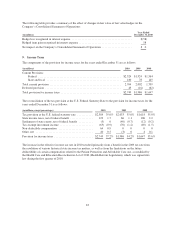

fair value measurement has been determined based on the lowest level input that is significant to the fair value

measurement in its entirety. The Company’s assessment of the significance of a particular item to the fair value

measurement in its entirety requires judgment, including the consideration of inputs specific to the asset or

liability.

The fair value hierarchy is as follows:

Level 1 — Quoted (unadjusted) prices for identical assets/liabilities in active markets.

Level 2 — Other observable inputs, either directly or indirectly, including:

• Quoted prices for similar assets/liabilities in active markets;

• Quoted prices for identical or similar assets in non-active markets (e.g., few transactions, limited

information, non-current prices, high variability over time);

• Inputs other than quoted prices that are observable for the asset/liability (e.g., interest rates, yield

curves, volatilities, default rates); and

• Inputs that are derived principally from or corroborated by other observable market data.

Level 3 — Unobservable inputs that cannot be corroborated by observable market data.

75