Under Armour 2006 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2006 Under Armour annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

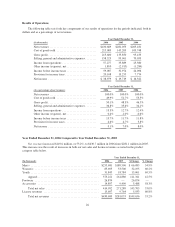

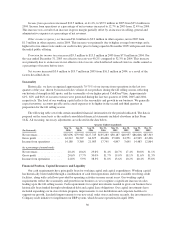

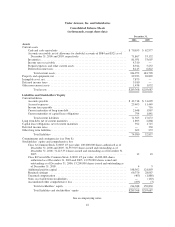

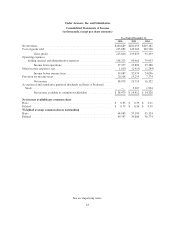

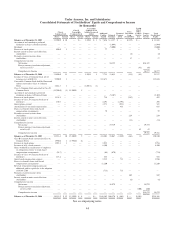

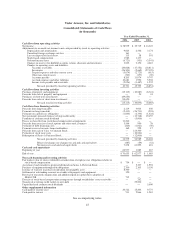

Sales Returns, Allowances and Discounts

We record reductions to revenue for estimated customer returns, allowances and discounts. We base our

estimates on historical rates of customer returns and allowances as well as the specific identification of

outstanding returns and allowances that have not yet been received by us. We record reductions to gross sales for

certain customer-based incentives, which include volume-based discounts and certain cooperative advertising

credits. We base our estimates for customer returns, allowances and discounts primarily on anticipated sales

volume throughout the year. The actual amount of customer returns, allowances and discounts, which is

inherently uncertain, may differ from our estimates. If we determined that actual or expected returns, allowances

or discounts were significantly greater or lower than the reserves we had established, we would record a

reduction or increase, as appropriate, to net sales in the period in which we made such a determination.

Reserve for Uncollectible Accounts Receivable

We make ongoing estimates relating to the collectibility of our accounts receivable and maintain a reserve

for estimated losses resulting from the inability of our customers to make required payments. In determining the

amount of the reserve, we consider our historical level of credit losses and make judgments about the

creditworthiness of significant customers based on ongoing credit evaluations. Because we cannot predict future

changes in the financial stability of our customers, actual future losses from uncollectible accounts may differ

from our estimates. If the financial condition of our customers were to deteriorate, resulting in their inability to

make payments, a larger reserve might be required. In the event we determined that a smaller or larger reserve

was appropriate, we would record a benefit or charge to selling, general and administrative expense in the period

in which we made such a determination.

Inventory Valuation and Reserves

We value our inventory at standard costs which approximates our landed cost, using the first-in, first-out

method of cost determination. Market value is estimated based upon assumptions made about future demand and

retail market conditions. If we determine that the estimated market value of our inventory is less than the

carrying value of such inventory, we provide a reserve for such difference as a charge to cost of goods sold to

reflect the lower of cost or market. If actual market conditions are less favorable than those projected by us,

further adjustments may be required that would increase our cost of goods sold in the period in which the

adjustments were recorded.

Long-Lived Assets

The acquisition of long-lived assets, including furniture and fixtures, office equipment, plant equipment,

leasehold improvements, computer hardware and software and in-store fixtures, is recorded at cost and this cost

is depreciated over the asset’s estimated useful life. We continually evaluate whether events and circumstances

have occurred that indicate the remaining estimated useful life of long-lived assets may warrant revision or that

the remaining balance may not be recoverable. These factors may include a significant deterioration of operating

results, changes in business plans or changes in anticipated cash flows. When factors indicate that an asset should

be evaluated for possible impairment, we review long-lived assets to assess recoverability from future operations

using undiscounted cash flows. Impairments are recognized in earnings to the extent that the carrying value

exceeds fair value.

Intangible Assets

Intangible assets that are determined to have a definite life are amortized over the asset’s estimated useful

life and are evaluated and measured for impairment in accordance with our Long-Lived Assets critical

accounting policy discussed above.

35