Ulta 2008 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2008 Ulta annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

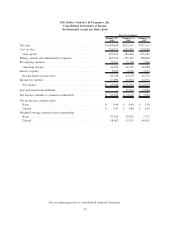

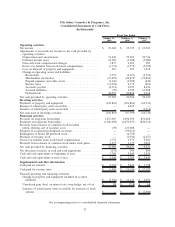

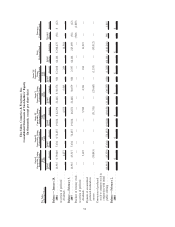

judgments that affect the reported amounts of our assets, liabilities, revenues and expenses. Management bases

estimates on historical experience and other assumptions it believes to be reasonable under the circumstances

and evaluates these estimates on an on-going basis. Actual results may differ from these estimates. A

discussion of our more significant estimates follows. Management has discussed the development, selection,

and disclosure of these estimates and assumptions with the audit committee of the board of directors.

Inventory valuation

Merchandise inventories are carried at the lower of average cost or market value. Cost is determined using the

weighted-average cost method and includes costs incurred to purchase and distribute goods as well as related

vendor allowances including co-op advertising, markdowns, and volume discounts. We record valuation

adjustments to our inventories if the cost of a specific product on hand exceeds the amount we expect to

realize from the ultimate sale or disposal of the inventory. These estimates are based on management’s

judgment regarding future demand, age of inventory, and analysis of historical experience. If actual demand or

market conditions are different than those projected by management, future merchandise margin rates may be

unfavorably or favorably affected by adjustments to these estimates.

Inventories are adjusted for the results of periodic physical inventory counts at each of our locations. We

record a shrink reserve representing management’s estimate of inventory losses by location that have occurred

since the date of the last physical count. This estimate is based on management’s analysis of historical results

and operating trends.

Adjustments to earnings resulting from revisions to management’s estimates of the lower of cost or market and

shrink reserves have been insignificant during fiscal 2008, 2007 and 2006.

Self-insurance

We are self-insured for certain losses related to health, workers’ compensation, and general liability insurance.

We maintain stop loss coverage with third-party insurers to limit our liability exposure. Current stop loss

coverage is $150,000 for health claims, $100,000 for general liability claims, and $250,000 for workers’

compensation claims. Management estimates undiscounted loss reserves associated with these liabilities in part

by considering historical claims experience, industry factors, and other actuarial assumptions including

information provided by third parties. Self-insurance reserves for fiscal 2008, 2007 and 2006 were $1.9 million,

$2.4 million and $2.3 million, respectively. Adjustments to earnings resulting from revisions to management’s

estimates of these reserves have been insignificant for fiscal 2008, 2007, and 2006.

Impairment of long-lived tangible assets

We review long-lived tangible assets whenever events or circumstances indicate these assets might not be

recoverable based on undiscounted future cash flows. Assets are reviewed at the lowest level for which cash

flows can be identified, which is the store level. Significant estimates are used in determining future operating

results of each store over its remaining lease term. If such assets are considered to be impaired, the impairment

to be recognized is measured by the amount by which the carrying amount of the assets exceeds the fair value

of the assets. We have not recorded an impairment charge in any of the periods presented in the accompanying

consolidated financial statements.

Share-based compensation

Effective January 29, 2006, we adopted the fair value recognition and measurement provisions of Statement of

Financial Accounting Standards (SFAS) No. 123(R), Share-Based Payment. Pursuant to SFAS No. 123(R),

share-based compensation cost is measured at grant date, based on the fair value of the award, and is

recognized as expense over the requisite service period for awards expected to vest. As a non-public entity

that previously used the minimum value method for pro forma disclosure purposes under SFAS No. 123, we

were required to adopt the prospective method of accounting under SFAS No. 123(R). Under this transitional

method, we record compensation expense in the consolidated statements of income for all awards granted after

42