TJ Maxx 1999 Annual Report Download - page 9

Download and view the complete annual report

Please find page 9 of the 1999 TJ Maxx annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

|

|

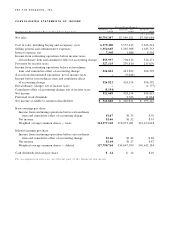

1999 of $5.2 million (net of income taxes of $3.4 million), or $.02 per share, is shown as the cumulative effect

of accounting change in the Consolidated Statements of Income.The accounting change has virtually no impact

on annual sales and earnings (before cumulative effect).However, due to the seasonal influences of the business,

the accounting change results in a shift of sales and earnings among the Company’s quarterly periods.As a result,

the Company has restated its earnings for the first three quarters of the fiscal year ended January 29, 2000 (see

Selected Quarterly Financial Data, page 45, for more information). Except for the Selected Quarterly Financial

Data, the Company has not presented pro forma results for prior fiscal years due to immateriality.

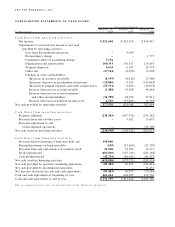

B . D i sp o sit io n s a nd A c q u i s i t i o n s

S a le o f C h ad w ick ’s o f Bo sto n : The Company sold its former Chadwick’s division in fiscal 1997 to Brylane,

Inc.As part of the proceeds from the sale, the Company received a $20 million convertible note. During fiscal

1998, the Company converted a portion of the Brylane note into 352,908 shares of Brylane, Inc. common stock

which it sold for $15.7 million. This sale resulted in an after-tax gain of $3.6 million. During fiscal 1999, the

balance of the note was converted into shares of Brylane common stock.A portion of the shares were donated

to the Company’s charitable foundation, and the remaining shares were sold. The net pre-tax impact of these

transactions was immaterial. Pursuant to the agreement, the Company retained the Chadwick’s consumer credit

card receivables. The cash provided by discontinued operations for fiscal 1998 represents the collection of the

remaining balance of the Chadwick’s consumer credit card receivables outstanding as of January 25, 1997.Also

pursuant to the disposition, the Company agreed to purchase certain amounts of excess inventory from Chad-

wick’s.This arrangement has subsequently been amended and extended through fiscal 2002.

S a le o f H it o r M iss: Effective September 30, 1995, the Company sold its Hit or Miss division to members of

Hit or Miss management and outside investors.The Company received $3.0 million in cash and a seven-year $10

million note with interest at 10%. During fiscal 1998, the Company forgave a portion of this note and was

released from certain obligations and guarantees which reduced the note to $5.5 million. During fiscal 1999,the

Company settled the note for $2.0 million, the balance of $3.5 million was charged to selling, general and

administrative expenses.

A cqu isit io n o f M a rsha lls: On November 17, 1995, the Company acquired the Marshalls family apparel

chain from Melville Corp o rat i o n .The Company paid $424.3 million in cash and $175 million in junior conve r t i bl e

p re fe r red stock.The total purchase price of Mars h a l l s , including acquisition costs of $6.7 million, was $606 million.

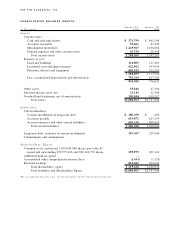

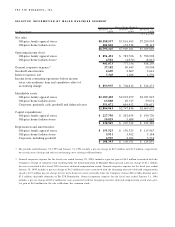

C . L o n g- Te rm D e b t a n d C re d it L i n e s

At January 29, 2000 and January 30, 1999, long-term debt, exclusive of current installments, consisted of the

following: Ja n u a ry 2 9, Ja nua ry 3 0 ,

I n Th o u s a n d s 2 0 0 0 1 9 9 9

Equipment notes, interest at 11% to 11.25% maturing

December 12, 2000 to December 30, 2001 $ 73 $ 433

General corporate debt:

Medium term notes, interest at 5.87% to 7.97% , $15 million maturing

October 21, 2003 and $5 million maturing September 20, 2004 20,000 20,000

65/8% unsecured notes, maturing June 15, 2000 –100,000

7% unsecured notes, maturing June 15, 2005 (effective interest rate of 7.02%

after reduction of the unamortized debt discount of $75,000 and $89,000

in fiscal 2000 and 1999, respectively) 99,925 99,911

7.45% unsecured notes, maturing December 15, 2009 (effective interest rate of

7.50% after reduction of unamortized debt discount of $631,000 in fiscal 2000) 199,369 –

Total general corporate debt 319,294 219,911

Long-term debt, exclusive of current installments $319,367 $220,344