Royal Caribbean Cruise Lines 2005 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2005 Royal Caribbean Cruise Lines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48

|

|

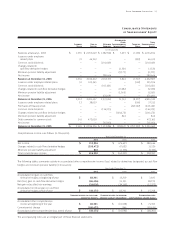

Note 10. Financial Instruments

The estimated fair values of our financial instruments are as follows

(in thousands):

2005 2004

Cash and cash equivalents $ 125,385 $ 628,578

Long-term debt

(including current portion

of long-term debt) (4,368,874) (6,580,079)

Foreign currency forward

contracts in a net (loss)

gain position (115,415) 104,904

Interest rate swap

agreements in a net

receivable position 8,456 20,267

Fuel swap agreements in

a net (payable) receivable

position (78) 8,130

The reported fair values are based on a variety of factors and

assumptions. Accordingly, the fair values may not represent actual

values of the financial instruments that could have been realized as

of December 31, 2005 or 2004 or that will be realized in the future

and do not include expenses that could be incurred in an actual sale

or settlement. Our financial instruments are not held for trading or

speculative purposes.

Our exposure under foreign currency contracts, interest rate and fuel

swap agreements is limited to the cost of replacing the contracts in

the event of non-performance by the counterparties to the contracts,

all of which are currently our lending banks. To minimize this risk, we

select counterparties with credit risks acceptable to us and we limit

our exposure to an individual counterparty. Furthermore, all foreign

currency forward contracts are denominated in primary currencies.

The carrying amounts of cash and cash equivalents approximate

their fair values due to the short maturity of these instruments.

The fair values of our senior notes, senior debentures, Liquid Yield

Option™ Notes and zero coupon convertible notes were estimated

by obtaining quoted market prices. The fair values of all other debt

were estimated using discounted cash flow analyses based on mar-

ket rates available to us for similar debt with the same remaining

maturities.

The fair values of our foreign currency forward contracts were esti-

mated using current market prices for similar instruments. Our expo-

sure to market risk for fluctuations in foreign currency exchange

rates relates to four ship construction contracts and forecasted

transactions. We use foreign currency forward contracts to mitigate

the impact of fluctuations in foreign currency exchange rates. As of

December 31, 2005, we had foreign currency forward contracts in a

notional amount of $2.6 billion maturing through 2008. The fair

value of our foreign currency forward contracts related to three ship

construction contracts, designated as fair value hedges, was a net

unrealized loss of approximately $103.4 million and a net unrealized

gain of approximately $34.7 million at December 31, 2005 and

2004, respectively. The fair value of our foreign currency forward

contracts related to the other ship construction contract, designated

as cash flow hedges, was an unrealized loss, of approximately $7.8

million and an unrealized gain of approximately $76.2 million at

December 31, 2005 and 2004, respectively. At December 31, 2005,

approximately 6% of the aggregate cost of the four ship contracts

was exposed to fluctuations in the euro exchange rate. (See Note 13.

Subsequent Events.

)

The fair values of our interest rate swap agreements were estimated

based on quoted market prices for similar or identical financial

instruments to those we hold. Our exposure to market risk for

changes in interest rates relates to our long-term debt obligations

and our operating lease for

Brilliance of the Seas

. We enter into

interest rate swap agreements to modify our exposure to interest

rate movements and to manage our interest expense and rent

expense.

Market risk associated with our long-term fixed rate debt is the

potential increase in fair value resulting from a decrease in interest

rates. As of December 31, 2005, we had interest rate swap agree-

ments, designated as fair value hedges, which exchanged fixed

interest rates for floating interest rates in a notional amount of

$268.8 million, maturing in 2006 through 2013.

Market risk associated with our long-term floating rate debt is the

potential increase in interest expense from an increase in interest

rates. As of December 31, 2005, we had an interest rate swap agree-

ment, designated as a cash flow hedge, which, exchanges floating

rate term debt for a fixed interest rate of 4.395% in a notional

amount of $25.0 million, maturing in 2008.

Market risk associated with our operating lease for

Brilliance of the

Seas

is the potential increase in rent expense from an increase in

sterling LIBOR rates. As of January 2006, we have effectively

changed 69% of the operating lease obligation from a floating rate

to a fixed rate obligation with a weighted-average rate of 4.83%

through a combination of interest rate swap agreements, designated as

cash flow hedges, and rate fixings with the lessor, maturing in 2012.

Royal Caribbean Cruises Ltd. 41

Notes to the Consolidated

Financial Statements (continued)