Konica Minolta 2007 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 2007 Konica Minolta annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

|

|

06

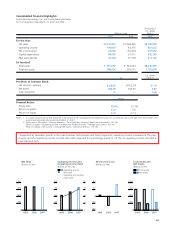

Strategies by Segment

In liquid crystal display (LCD)-use triacetyl cellulose film (TAC film) for polarizing

plate protection, we aim to expand the business on growing demand mainly for

high value-added viewing angle expansion film used in large LCDs in keeping

with the shift to large screen LCDs and higher resolution.

In optical pickup lenses, the Group will maintain a commanding market share

in next generation pickup lenses, and has already begun production of both Blu-

ray Disk and the high definition (HD) DVD formats. Materials development is the

key point for next generation pickup lenses, and the Konica Minolta merger has

created an advantage in the Group having both the design and production

technology to integrate plastic lens with glass molding technologies, resulting in

the ability to fully leverage these strengths to ensure commanding competitiveness.

Demand for glass hard disks is expanding because of stable growth in the lap-

top PC market and expanding applications such as networked home appliances

with hard disk drives. Responding to the growing demand, Konica Minolta is

expanding manufacturing capacity through overseas production.

In micro cameras units for camera-equipped mobile phones, we intend to

establish cost competitiveness in order to cope with intensified price competition

in the end product market.

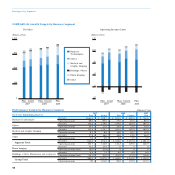

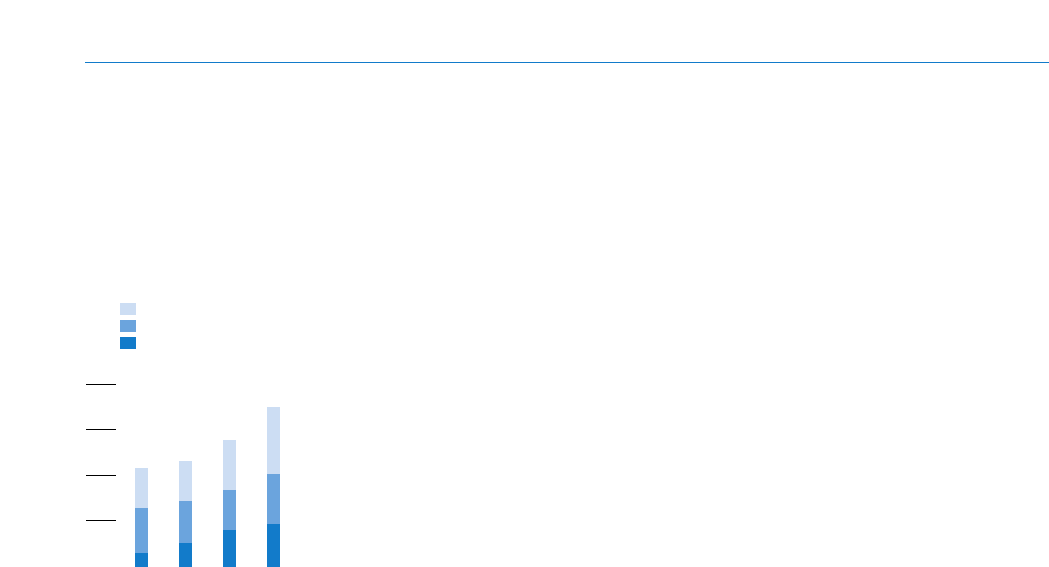

0

40

80

120

160

2004 2005 2006 2007

Net Sales

—

Subsegment

(Billions of Yen)

Display Materials

Memory Devices

Image Input/Output Devices

Optics