JetBlue Airlines 2006 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2006 JetBlue Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

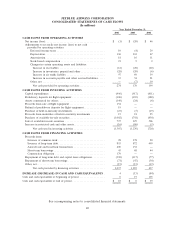

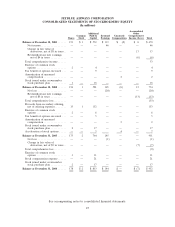

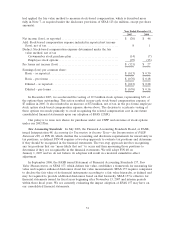

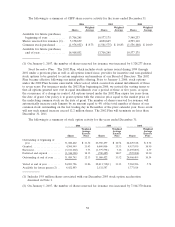

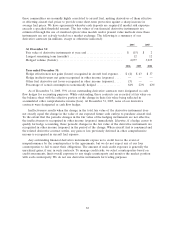

Note 6—Earnings (Loss) Per Share

The following table shows how we computed basic and diluted earnings (loss) per common share

for the years ended December 31 (dollars in millions; share data in thousands):

2006 2005 2004

Numerator:

Net income (loss) applicable to common stockholders . . . $ (1) $ (20) $ 46

Denominator:

Weighted-average shares outstanding for basic earnings

(loss) per share ..................................... 175,113 159,889 154,769

Effect of dilutive securities:

Employee stock options.............................. — — 11,403

Unvested common stock ............................. — — 42

Adjusted weighted-average shares outstanding and

assumed conversions for diluted earnings (loss)

per share........................................... 175,113 159,889 166,214

For each of the years ended December 31, 2006 and 2005, a total 20.8 million shares issuable

upon conversion of our convertible debt were excluded from the diluted earnings per share calculation

since the assumed conversion would be anti-dilutive. We also excluded 31.1 million shares in each of

the years ended December 31, 2006 and 2005, and 7.6 million shares issuable upon exercise of

outstanding stock options for the year ended December 31, 2004, from the diluted earnings (loss) per

share computation since their exercise price was greater than the average market price of our common

stock or they were otherwise anti-dilutive.

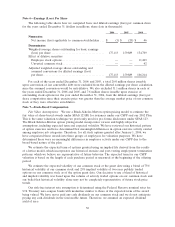

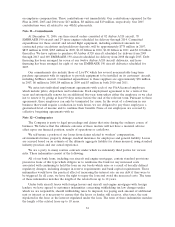

Note 7—Stock-Based Compensation

Fair Value Assumptions: We use a Black-Scholes-Merton option pricing model to estimate the

fair value of share-based awards under SFAS 123(R) for issuances under our CSPP and our 2002 Plan.

This is the same valuation technique we previously used for pro forma disclosures under SFAS 123.

The Black-Scholes-Merton option pricing model incorporates various and highly subjective

assumptions, including expected term and expected volatility. We have reviewed our historical pattern

of option exercises and have determined that meaningful differences in option exercise activity existed

among employee job categories. Therefore, for all stock options granted after January 1, 2006, we

have categorized these awards into three groups of employees for valuation purposes. We have

determined there were no meaningful differences in employee activity under our CSPP due to the

broad-based nature of the plan.

We estimate the expected term of options granted using an implied life derived from the results

of a lattice model, which incorporates our historical exercise and post-vesting employment termination

patterns, which we believe are representative of future behavior. The expected term for our CSPP

valuation is based on the length of each purchase period as measured at the beginning of the offering

period.

We estimate the expected volatility of our common stock at the grant date using a blend of 75%

historical volatility of our common stock and 25%implied volatility of two-year publicly traded

options on our common stock as of the option grant date. Our decision to use a blend of historical

and implied volatility was based upon the volume of actively traded options on our common stock and

our belief that historical volatility alone may not be completely representative of future stock price

trends.

Our risk-free interest rate assumption is determined using the Federal Reserve nominal rates for

U.S. Treasury zero-coupon bonds with maturities similar to those of the expected term of the award

being valued. We have never paid any cash dividends on our common stock and we do not anticipate

paying any cash dividends in the foreseeable future. Therefore, we assumed an expected dividend

yield of zero.

56