JetBlue Airlines 2006 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2006 JetBlue Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

Income Taxes: We account for income taxes utilizing the liability method. Deferred income taxes

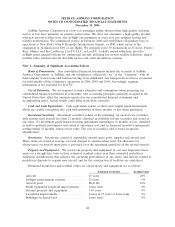

are recognized for the tax consequences of temporary differences between the tax and financial

statement reporting bases of assets and liabilities. A valuation allowance for net deferred tax assets is

provided unless realizability is judged by us to be more likely than not.

Stock-Based Compensation: Effective January 1, 2006, we adopted the provisions of Statement of

Financial Accounting Standards 123(R), Share-Based Payment, and related interpretations, or SFAS

123(R), to account for stock-based compensation using the modified prospective transition method

and therefore will not restate our prior period results. SFAS 123(R) supersedes Accounting Principles

Board Opinion 25, Accounting for Stock Issued to Employees, or APB 25, and revises guidance in

Statement of Financial Accounting Standards 123, Accounting for Stock-Based Compensation,orSFAS

123. Among other things, SFAS 123(R) requires that compensation expense be recognized in the

financial statements for share-based awards based on the grant date fair value of those awards. The

modified prospective transition method applies to (a) unvested stock options under our 2002 Stock

Incentive Plan, or the 2002 Plan, and issuances under our Crewmember Stock Purchase Plan, or CSPP,

outstanding as of December 31, 2005 based on the grant date fair value estimated in accordance with

the pro forma provisions of SFAS 123, and (b) any new share-based awards granted subsequent to

December 31, 2005, based on the grant-date fair value estimated in accordance with the provisions of

SFAS 123(R). Additionally, stock-based compensation expense includes an estimate for pre-vesting

forfeitures and is recognized over the requisite service periods of the awards on a straight-line basis,

which is generally commensurate with the vesting term.

Prior to January 1, 2006, we accounted for our stock-based compensation plans in accordance

with APB 25 and related interpretations. Accordingly, compensation expense for a stock option grant

was recognized only if the exercise price was less than the market value of our common stock on the

grant date. Compensation expense was not recognized under our CSPP as the purchase price of the

stock issued thereunder was not less than 85%of the lower of the fair market value of our common

stock at the beginning of each offering period or at the end of each purchase period under the plan.

Prior to our adoption of SFAS 123(R), as required under the disclosure provisions of SFAS 123, as

amended, we provided pro forma net income (loss) and earnings (loss) per common share for each

period as if we had applied the fair value method to measure stock-based compensation expense.

SFAS 123(R) requires the benefits associated with tax deductions in excess of recognized

compensation cost to be reported as a financing cash flow rather than as an operating cash flow as

previously required. In 2006, we did not record any excess tax benefit generated from option exercises.

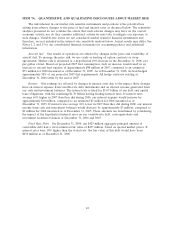

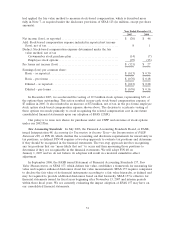

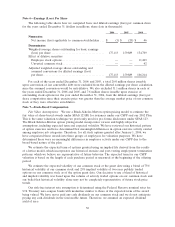

The table below summarizes the impact on our results of operations for the year ended

December 31, 2006 of outstanding stock options under our 2002 Plan and issuances under our CSPP

recognized under the provisions of SFAS 123(R) (in millions, except per share data):

2006

Stock-based compensation expense:

Issuances under crewmember stock purchase plan . . $ 13

Employee stock options ......................... 8

Income tax expense .............................. (4)

Decrease in net income (loss)...................... $ 17

Decrease in earnings (loss) per common share:

Basic ......................................... $ 0.09

Diluted ....................................... $ 0.09

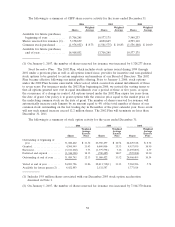

Prior to our adoption of SFAS 123(R), we presented unearned compensation as a separate

component of stockholders’ equity. In accordance with the provisions of SFAS 123(R), on

January 1, 2006, we reclassified unearned compensation to additional paid-in capital on our balance

sheet. The following table illustrates the effect on net income and earnings per common share as if we

50