JetBlue Airlines 2006 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2006 JetBlue Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

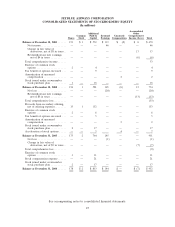

|

|

appropriateness of the estimates that are required to prepare our financials statements. We believe

that our estimates and judgments are reasonable; however, actual results and the timing of recognition

of such amounts could differ from those estimates. In addition, estimates routinely require adjustment

based on changing circumstances and the receipt of new or better information.

Critical accounting policies and estimates are defined as those that are reflective of significant

judgments and uncertainties, and potentially result in materially different results under different

assumptions and conditions. The policies and estimates discussed below have been reviewed with our

independent registered public accounting firm and with the Audit Committee of our Board of

Directors. For a discussion of these and other accounting policies, see Note 1 to our consolidated

financial statements.

Passenger revenue. Passenger ticket sales are initially recorded as a component of air traffic

liability. Revenue is recognized when transportation is provided or when a ticket or customer credit

expires, as all of our tickets are non-refundable. Upon payment of a change fee, we provide our

customers with a credit that is recorded in air traffic liability, which expires 12 months from the date

of scheduled travel if not used.

Accounting for long-lived assets. In accounting for long-lived assets, we make estimates about

the expected useful lives, projected residual values and the potential for impairment. In estimating

useful lives and residual values of our aircraft, we have relied upon actual industry experience with

the same or similar aircraft types and our anticipated utilization of the aircraft. Changing market

prices of new and used aircraft, government regulations and changes in our maintenance program or

operations could result in changes to these estimates. The amortization of our purchased technology,

which resulted from our acquisition of LiveTV in 2002, is based on the average number of aircraft in

service and expected to be in service as of the date of their acquisition. This method results in an

increasing annual expense through 2009 when the last of these aircraft are expected to be placed into

service and is adjusted to reflect changes in our contractual delivery schedule.

Our long-lived assets are evaluated for impairment at least annually or when events and

circumstances indicate that the assets may be impaired. Indicators include operating or cash flow

losses, significant decreases in market value or changes in technology. As our assets are all relatively

new and we continue to have positive cash flow, we have not identified any significant impairments

related to our long-lived assets at this time.

Stock-based compensation. The adoption of SFAS 123(R) in 2006 required the recording of

stock-based compensation expense for issuances under our stock purchase plan and stock option plan

over their requisite service period using a fair value approach similar to the pro forma disclosure

requirements of Statement of Financial Accounting Standards No. 123, Accounting for Stock-Based

Compensation, or SFAS 123. We use a Black-Scholes-Merton option pricing model to estimate the fair

value of share-based awards under SFAS 123(R), which is the same valuation technique we previously

used for pro forma disclosures under SFAS 123. The Black-Scholes-Merton option pricing model

incorporates various and highly subjective assumptions. We estimate the expected term of options

granted using an implied life derived from the results of a lattice model, which incorporates our

historical exercise and post-vesting cancellation patterns, which we believe are representative of future

behavior. The expected term for our employee stock purchase plan valuation is based on the length of

each purchase period as measured at the beginning of the offering period. We estimate the expected

volatility of our common stock at the grant date using a blend of 75%historical volatility of our

common stock and 25%implied volatility of two-year publicly traded options on our common stock as

of the option grant date. Our decision to use a blend of historical and implied volatility was based

upon the volume of actively traded options on our common stock and our belief that historical

volatility alone may not be completely representative of future stock price trends. Regardless of the

method selected, significant judgment is required for some of the valuation variables. The most

significant of these is the volatility of our common stock and the estimated term over which our stock

options will be outstanding. The valuation calculation is sensitive to even slight changes in these

estimates.

40