GE 2007 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2007 GE annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

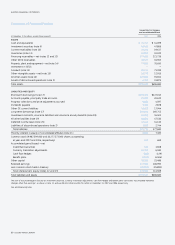

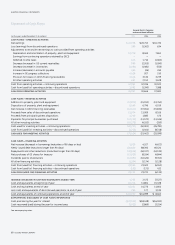

58 ge 2007 annual report

’

During 2007, GECS and GECS affi liates issued $84.6 billion of

senior, unsecured long-term debt and $5.7 billion of subordinated

debt. This debt was both fi xed and fl oating rate and was issued

to institutional and retail investors in the U.S. and 17 other global

markets. Maturities for these issuances ranged from one to 60

years. We used the proceeds primarily for repayment of maturing

long-term debt, but also to fund acquisitions and organic growth.

We anticipate that we will issue approximately $80 billion of

long-term debt during 2008. The ultimate amount we issue will

depend on our needs and on market conditions.

We target a ratio for commercial paper not to exceed 35% of

outstanding debt based on the anticipated composition of our

assets and the liquidity profi le of our debt. GE Capital is the most

widely held name in global commercial paper markets.

We continue to believe that alternative sources of liquidity are

suffi cient to permit an orderly transition from commercial paper in

the unlikely event of impaired access to those markets. Funding

sources on which we would rely would depend on the nature of

such a hypothetical event, but include $64.8 billion of contractually

committed lending agreements with 72 highly-rated global banks

and investment banks. Total credit lines extending beyond one

year increased $5.0 billion to $64.8 billion at December 31, 2007.

See note 17.

Beyond contractually committed lending agreements, other

sources of liquidity include medium and long-term funding,

monetization, asset securitization, cash receipts from our lending

and leasing activities, short-term secured funding on global

assets and potential sales of other assets.

PRINCIPAL DEBT CONDITIONS are described below.

The following conditions relate to GE and GECS:

• Swap, forward and option contracts are required to be exe-

cuted under standard master-netting agreements containing

mutual downgrade provisions that provide the ability of the

counterparty to require assignment or termination if the long-

term credit rating of either GE or GECS were to fall below A–/

A3. Our related obligation, net of master-netting agreements

would have been $3.4 billion at December 31, 2007.

• If GE Capital’s ratio of earnings to fi xed charges, which was

1.56:1 at the end of 2007, were to deteriorate to 1.10:1, GE

has committed to contribute capital to GE Capital. GE also

guaranteed certain issuances of GECS subordinated debt

having a face amount of $0.8 billion at December 31, 2007

and 2006.

• In connection with certain subordinated debentures for

which GECS receives equity credit by rating agencies, GE has

agreed to forego dividends, distributions or other payments

from GECS during events of default or interest extensions

under such subordinated debentures. There were $8.1 billion

of such debentures outstanding at December 31, 2007.

The following conditions relate to consolidated entities.

• If the short-term credit rating of GE Capital or certain consoli-

dated entities discussed further in note 27 were to be reduced

below A–1/P–1, GE Capital would be required to provide sub-

stitute liquidity for those entities or provide funds to retire

the outstanding commercial paper. The maximum net amount

that GE Capital would be required to provide in the event of

such a downgrade is determined by contract, and amounted

to $7.2 billion at January 1, 2008.

• One group of consolidated entities holds high quality invest-

ment securities funded by the issuance of GICs. If the long-

term credit rating of GE Capital were to fall below AA–/Aa3

or its short-term credit rating were to fall below A–1+/P–1,

GE Capital could be required to provide up to $6.2 billion of

capital to such entities.

In our history, we have never violated any of the above conditions

at GE, GECS or GE Capital. We believe that under any reasonable

future economic developments, the likelihood that any such

arrangements could have a signifi cant effect on our operations,

cash fl ows or fi nancial position is remote.

Critical Accounting Estimates

Accounting estimates and assumptions discussed in this section

are those that we consider to be the most critical to an under-

standing of our fi nancial statements because they inherently

involve signifi cant judgments and uncertainties. For all of these

estimates, we caution that future events rarely develop exactly

as forecast, and the best estimates routinely require adjustment.

Also see note 1, Summary of Signifi cant Accounting Policies,

which discusses the signifi cant accounting policies that we have

selected from acceptable alternatives.

LOSSES ON FINANCING RECEIVABLES are recognized when they

are incurred, which requires us to make our best estimate of

probable losses inherent in the portfolio. Such estimate requires

consideration of historical loss experience, adjusted for current

conditions, and judgments about the probable effects of relevant

observable data, including present economic conditions such

as delinquency rates, fi nancial health of specifi c customers and

market sectors, collateral values, and the present and expected

future levels of interest rates. Our risk management process,

which includes standards and policies for reviewing major risk

exposures and concentrations, ensures that relevant data are

identifi ed and considered either for individual loans or fi nancing

leases, or on a portfolio basis, as appropriate.

Our lending and leasing experience and the extensive data

we accumulate and analyze facilitate estimates that have proven

reliable over time. Our actual loss experience was in line with

expectations for 2007, 2006 and 2005. While Commercial Finance

continues to experience strong credit quality, we currently expect

higher delinquencies in the GE Money U.S. portfolio.