United Healthcare 2009 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2009 United Healthcare annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

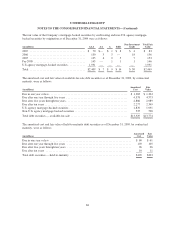

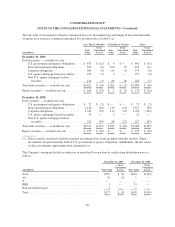

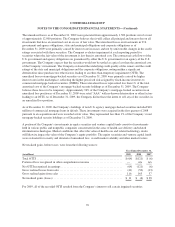

UNITEDHEALTH GROUP

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

5. Fair Value

Fair values of available-for-sale debt and equity securities are based on quoted market prices, where available.

The Company obtains one price for each security primarily from a third party pricing service (pricing service),

which generally uses quoted or other observable inputs for the determination of fair value. The pricing service

normally derives the security prices through recently reported trades for identical or similar securities, making

adjustments through the reporting date based upon available observable market information. For securities not

actively traded, the pricing service may use quoted market prices of comparable instruments or discounted cash

flow analyses, incorporating inputs that are currently observable in the markets for similar securities. Inputs that

are often used in the valuation methodologies include, but are not limited to, non-binding broker quotes,

benchmark yields, credit spreads, default rates and prepayment speeds. As the Company is responsible for the

determination of fair value, it performs quarterly analyses on the prices received from the pricing service to

determine whether the prices are reasonable estimates of fair value. Specifically, the Company compares the

prices received from the pricing service to prices reported by its custodian, its investment consultant and third

party investment advisors. Additionally, the Company compares changes in the reported market values and

returns to relevant market indices to test the reasonableness of the reported prices. Based on the Company’s

internal price verification procedures and review of fair value methodology documentation provided by

independent pricing services, the Company has not historically adjusted the prices obtained from the pricing

service.

In instances in which the inputs used to measure fair value fall into different levels of the fair value hierarchy, the

fair value measurement has been determined based on the lowest level input that is significant to the fair value

measurement in its entirety. The Company’s assessment of the significance of a particular item to the fair value

measurement in its entirety requires judgment, including the consideration of inputs specific to the asset.

The fair value hierarchy is as follows:

Level 1 — Quoted (unadjusted) prices for identical assets in active markets.

Level 2 — Other observable inputs, either directly or indirectly, including:

• Quoted prices for similar assets in active markets;

• Quoted prices for identical or similar assets in non-active markets (e.g., few transactions, limited

information, non-current prices, high variability over time, etc.);

• Inputs other than quoted prices that are observable for the asset (e.g., interest rates, yield curves,

volatilities, default rates, etc.); and

• Inputs that are derived principally from or corroborated by other observable market data.

Level 3 — Unobservable inputs that cannot be corroborated by observable market data.

71