Under Armour 2012 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2012 Under Armour annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

or changes in anticipated cash flows. When factors indicate that an asset should be evaluated for possible

impairment, we review long-lived assets to assess recoverability from future operations using undiscounted cash

flows. If future undiscounted cash flows are less than the carrying value, an impairment is recognized in earnings

to the extent that the carrying value exceeds fair value.

Indefinite lived intangible assets are not amortized and are required to be tested for impairment at least

annually or sooner whenever events or changes in circumstances indicate that the assets may be impaired. We

perform intangible asset impairment tests in the fourth quarter of each fiscal year. No material impairments were

recorded related to long-lived assets or indefinite lived intangible assets during the years ended December 31,

2012, 2011 and 2010.

Income Taxes

Income taxes are accounted for under the asset and liability method. Deferred income tax assets and

liabilities are established for temporary differences between the financial reporting basis and the tax basis of our

assets and liabilities at tax rates expected to be in effect when such assets or liabilities are realized or settled.

Deferred income tax assets are reduced by valuation allowances when necessary.

Assessing whether deferred tax assets are realizable requires significant judgment. We consider all available

positive and negative evidence, including historical operating performance and expectations of future operating

performance. The ultimate realization of deferred tax assets is often dependent upon future taxable income and

therefore can be uncertain. To the extent we believe it is more likely than not that all or some portion of the asset

will not be realized, valuation allowances are established against our deferred tax assets, which increase income

tax expense in the period when such a determination is made.

Income taxes include the largest amount of tax benefit for an uncertain tax position that is more likely than

not to be sustained upon audit based on the technical merits of the tax position. Settlements with tax authorities,

the expiration of statutes of limitations for particular tax positions, or obtaining new information on particular tax

positions may cause a change to the effective tax rate. We recognize accrued interest and penalties related to

unrecognized tax benefits in the provision for income taxes on the consolidated statements of income.

Stock-Based Compensation

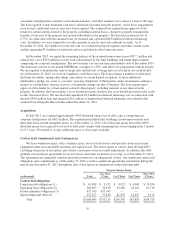

We account for stock-based compensation in accordance with accounting guidance that requires all stock-

based compensation awards granted to employees and directors to be measured at fair value and recognized as an

expense in the financial statements. As of December 31, 2012, we had $24.5 million of unrecognized

compensation expense related to time-based awards expected to be recognized over a weighted average period of

2.7 years. As of December 31, 2012, we had an additional $4.2 million of unrecognized compensation expense

related to performance-based stock options expected to be recognized over a weighted average period of 1.1

years.

Determining the appropriate fair value model and calculating the fair value of stock-based compensation

awards require the input of highly subjective assumptions, including the expected life of the stock-based

compensation awards, stock price volatility and estimated forfeiture rates. We use the Black-Scholes option-

pricing model to determine the fair value of stock-based compensation awards. The assumptions used in

calculating the fair value of stock-based compensation awards represent management’s best estimates, but the

estimates involve inherent uncertainties and the application of management judgment. In addition, compensation

expense for performance-based awards is recorded over the related service period when achievement of the

performance target is deemed probable, which requires management judgment. For example, the achievement of

the operating income targets related to the performance-based restricted stock units granted in 2012 and a portion

of the awards granted in 2011 were not deemed probable as of December 31, 2012. Additional stock-based

compensation of up to $16.6 million would have been recorded in 2012 for these performance-based restricted

42