Rite Aid 2011 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2011 Rite Aid annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

|

|

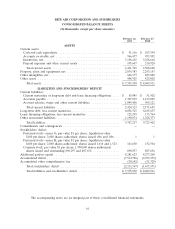

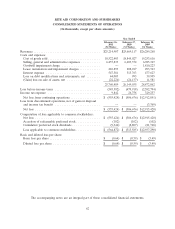

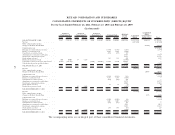

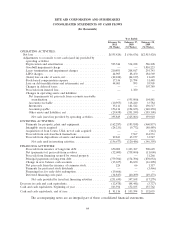

RITE AID CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

For the Years Ended February 26, 2011, February 27, 2010 and February 28, 2009

(In thousands, except per share amounts)

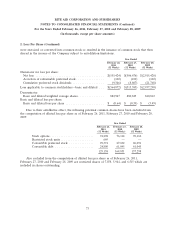

1. Summary of Significant Accounting Policies (Continued)

information not previously available. Due to the complexity of some of these uncertainties, the ultimate

resolution may result in a payment that is materially different from the current estimate of the tax

liabilities.

Sales Tax Collected

Sales taxes collected from customers and remitted to various governmental agencies are presented

on a net basis (excluded from revenues) in the Company’s statement of operations.

Use of Estimates

The preparation of the financial statements in conformity with accounting principles generally

accepted in the United States of America requires management to make estimates and assumptions

that affect the amounts reported in the financial statements and accompanying notes. Actual results

could differ from those estimates.

Significant Concentrations

The Company’s pharmacy sales were primarily to customers covered by health plan contracts,

which typically contract with a third party payor that agrees to pay for all or a portion of a customer’s

eligible prescription purchases. During fiscal 2011, the top five third party payors accounted for

approximately 60.9% of the Company’s pharmacy sales. The largest third party payor represented

23.8%, 21.2%, and 18.7% of pharmacy sales during fiscal 2011, 2010, and 2009, respectively. Third

party payors are entities such as an insurance company, governmental agency, health maintenance

organization or other managed care provider, and typically represent several health care contracts and

customers. During fiscal 2011, state sponsored Medicaid agencies accounted for approximately 11.5% of

the Company’s pharmacy sales, the largest of which was approximately 3.1% of the Company’s

pharmacy sales. During fiscal 2011, approximately 27.0% of the Company’s pharmacy sales were to

customers covered by Medicare Part D. Any significant loss of third-party payor business could have a

material adverse effect on the Company’s business and results of operations.

During fiscal 2011, the Company purchased brand pharmaceuticals and some generic

pharmaceuticals which amounted to approximately 91.4% of the dollar volume of its prescription drugs

from a single wholesaler, McKesson Corp. (‘‘McKesson’’), under a contract expiring April 1, 2013. With

limited exceptions, the Company is required to purchase all of its branded pharmaceutical products

from McKesson. If the Company’s relationship with McKesson was disrupted, the Company could have

temporary difficulty filling prescriptions for brand named drugs until a replacement wholesaler

agreement was executed, which would negatively impact the business. The Company purchases almost

all of its generic (non-brand name) pharmaceuticals directly from manufactures which account for

approximately 76% of its prescription volume. The loss of any one of the generic suppliers would not

disrupt the Company’s ability to fill generic (non-brand name) prescriptions but could negatively impact

the Company’s results.

71