Qantas 2007 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2007 Qantas annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

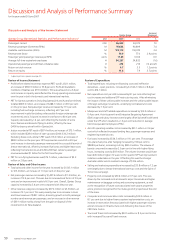

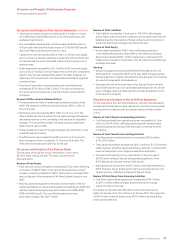

Review of Income Statement

Profit before related income tax expense (PBT) was $1,032.1 million,

an increase of $360.9 million or 53.8 per cent. Profit attributable to

members of Qantas was $719.4 million. This was achieved on a 3.4 per

cent increase in capacity and reflected the strong operating environment

over the year in both the domestic and international markets.

PBT for Qantas operations (including QantasLink and Australian Airlines)

totalled $865.0 million, an increase of $288.1 million or 49.9 per cent

on the prior year. Net passenger revenue increased by 11.5 per cent,

including fuel surcharge recoveries, reflecting a 8.7 per cent

improvement in yield (excluding unfavourable foreign exchange rate

movements) and a 3.4 point increase in seat factor to 80.6 per cent.

Capacity decreased by 1.4 per cent reflecting the transfer of some

trans-Tasman and domestic flying to Jetstar, offset by the new

Q400 turboprop aircraft within QantasLink.

Jetstar recorded a PBT result of $87.4 million, an increase of $75.1 million,

which included $28.0 million of start-up costs (2006: $14.2 million).

Excluding these costs, Jetstar’s PBT was $115.4 million, an increase of

$88.9 million on the prior year. PBT improved as a result of a 42.9 per

cent increase in domestic passenger revenue and the successful launch of

Jetstar International, offset by increased fuel costs and higher lease costs

reflecting the transition to an all A320-200 fleet. Jetstar’s passenger

revenue exceeded $1 billion for the first time this year.

PBT for non-flying businesses was $79.7 million, a decrease of $2.3

million or 2.8 per cent.

Review of Sales and Other Income

Total sales and other income for the year increased by $1,505.1 million

to $15.2 billion, an increase of 11.0 per cent on the prior year.

Net passenger revenue increased by $1,407.9 million to $11.9 billion, an

increase of 13.4 per cent. This was due to increased seat factor of 2.9 per

cent and an improvement in yield of 6.9 per cent. Overall, Qantas Group

capacity increased by 3.4 per cent compared with the prior year.

Other revenue categories increased by $97.2 million to $3.3 billion, an

increase of 3.1 per cent. This was primarily due to an increase in tours

and travel revenue of $48.1 million, driven by growth in both passenger

numbers and revenue per passenger, and an increase in other revenue

of $69.1 million mainly arising from the gain on disposal of the

investment in Air New Zealand.

•

•

•

•

•

•

•

Review of Expenditure

Total expenditure, including net financing costs and ineffective

derivatives – open positions, increased by $1,144.2 million or 8.8 per

cent to $14.1 billion.

Net expenditure cost per ASK increased by 8.1 per cent reflecting fuel

cost increases and additional SFP restructuring costs. After eliminating

the impact of these unfavourable increases and the unfavourable impact

of foreign exchange movements, underlying normalised unit costs

decreased by 1.9 per cent.

Manpower and staff related expenditure increased by $13.0 million or

0.4 per cent. Activity growth and Enterprise Bargaining Agreement

(EBA) wage and salary increases were largely offset by benefits delivered

under the SFP which resulted in a 1.6 per cent reduction in average

full-time equivalent employees (FTEs).

Aircraft operating variable costs increased by $91.1 million or 3.6 per

cent which reflected increased landing fees, passenger expenses and

engineering material costs.

Fuel costs increased by $534.5 million or 19.1 per cent. The average

into-plane fuel price after hedging increased by 19.8 per cent to

$88.89 per barrel, increasing costs by $555.0 million. The volume of

barrels consumed increased by 2.9 per cent in line with higher flying

hours, increasing costs by $93 million. The volume increase would have

been $45 million higher if it were not for specific SFP fuel improvement

initiatives undertaken in the year. Offsetting this was the stronger

Australian dollar which resulted in savings of $126 million.

Selling and marketing expenditure increased by $33.8 million or 7.2 per

cent largely due to Jetstar International start-up costs and the Spirit of

Tomorrow campaign.

Property costs increased by $30.4 million or 9.5 per cent. This was

driven by the increased rents at domestic airport terminals and higher

maintenance on baggage sorting and screening equipment, as well

as the recognition of future costs associated with vacant properties

and a provision recognised for the make-good of properties at the end

of the lease.

Computer and communication costs increased by $39.5 million or

8.1 per cent due to higher finance system implementation costs, an

increase in reservation fees associated with higher passenger volumes

and an increase in infrastructure costs following the closure of the

CBD Data Centre.

Tours and Travel costs increased by $50.5 million or 8.5 per cent in line

with increased Tours and Travel revenue.

•

•

•

•

•

•

•

•

•

Discussion and Analysis of the Income Statement

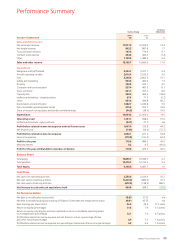

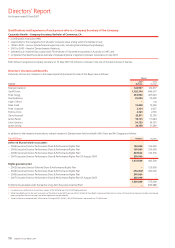

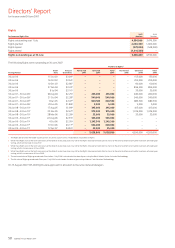

Qantas Group Operational Statistics and Performance Indicators1

Qantas Group

Increase/

(Decrease)

Unit 2007 2006 %

Passengers carried 000 36,449 34,075 7.0

Revenue passenger kilometres (RPKs) M 97,622 90,899 7.4

Available seat kilometres (ASKs) M 122,119 118 ,070 3.4

Revenue seat factor %79.9 77.0 2.9 points

Passenger yield (passenger revenue per RPK) cents 11.69 10.94 6.9

Average full-time equivalent employees # 34,267 34,832 (1.6)

Operational passenger aircraft fleet at balance date # 213 216 (3) aircraft

Return on total revenue % 4.7 3.5 1.2 points

Return on equity %11.6 7.9 3.7 points

A glossary of terms appears on page 141.

1

50 Qantas |Annual Report 2007

Discussion and Analysis of Performance Summary

for the year ended 30 June 2007