Porsche 2009 Annual Report Download - page 168

Download and view the complete annual report

Please find page 168 of the 2009 Porsche annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

|

|

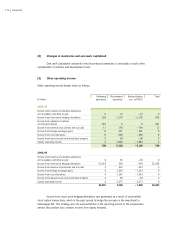

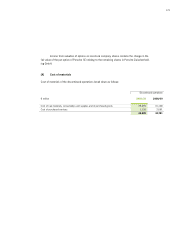

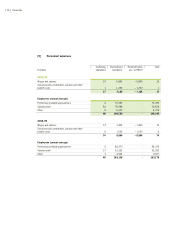

168 Financials

Amendments to IFRS 2 “Share-based Payment”

The amendment clarifies that only service and performance conditions constitute vesting

conditions. The amendment also provides that the rulings on premature termination apply regard-

less of whether the share-based payment plan is terminated by the company or another party.

Amendments to IAS 39 “Financial Instruments: Recognition and Measurement – Eligible Hedge Items”

This amendment specifies how the principles contained in IAS 39 are to be applied for the

hedge accounting in two specific situations. These are the unilateral risk with reference to a hedged

transaction (e.g. the risk of changes in the fair value or cash flows above or below a fixed price or

another variable) and the risk of inflation in a financially hedged transaction.

IAS 39 “Financial Instruments: Recognition and Measurement – Reclassification of Financial Assets –

Effective Date and Transition”

The amendment provides adjusted transitional rulings relating to the possibility of reclassi-

fying financial assets.

Amendment to IAS 32 “Financial Instruments: Presentation” and IAS 1 “Presentation of Financial

Statements”

The amendment mainly refers to the conditions for the classification of cancellable instru-

ments as equity or debt capital.

Amendments to IFRIC 9 “Reassessment of Embedded Derivatives” and IAS 39 “Financial Instruments:

Recognition and Measurement”

An entity has to check whether a derivative embedded in a host contract can be separated

if the whole hybrid instrument has been reclassified from the category at fair value through profit

and loss in accordance with the amendments to IAS 39 from October 2008. If the derivative has to

be accounted for separately but its fair value cannot be reliably determined or an entity cannot

perform the necessary assessment, the entire hybrid instrument has to remain in the category

financial instruments at fair value through profit and loss.

Annual improvements project II

The International Accounting Standards Board (IASB) published the “Improvements to IFRSs”

in April 2009. Most of the amendments are clarifications or corrections to existing IFRSs or chan-

ges resulting from modifications already made to IFRSs. Some of the clarifications and corrections

are applicable to the consolidated financial statements for 2009/10 on account of their specific

transitional requirements.