Porsche 2009 Annual Report Download - page 156

Download and view the complete annual report

Please find page 156 of the 2009 Porsche annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

|

|

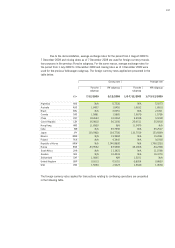

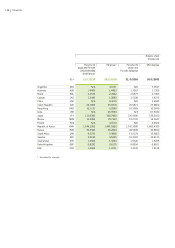

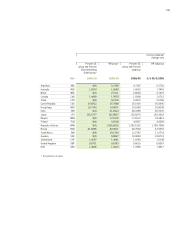

156 Financials

Financial instruments

According to IAS 39, a financial instrument is any contract that gives rise to a financial as-

set at one entity and a financial liability or equity instrument at another entity. If the trade date of a

financial asset differs from the settlement date, it is initially accounted for at the settlement date.

Initial recognition of a financial instrument is at fair value. Transaction costs are included for finan-

cial instruments not designated as at fair value through profit or loss. Subsequent measurement of

financial instruments is either at fair value or amortized cost depending on their category. Each

financial instrument is allocated to a category upon initial recognition.

With respect to measurement, IAS 39 distinguishes between the following categories of financial

assets:

· Financial assets at fair value through profit or loss (FVtPL) and held for trading (HfT)

· Held-to-maturity investments (HtM)

· Available-for-sale financial assets (AfS)

· Loans and receivables (LaR)

Financial liabilities are divided into the two categories:

· Financial liabilities at fair value through profit or loss (FVtPL) and held for trading (HfT)

· Financial liabilities measured at amortized cost (FLAC)

Depending on the category, measurement of financial instruments is either at fair value or

amortized cost.

Fair value corresponds to market price provided the financial instruments measured are

traded on an active market. If there is no active market for a financial instrument, fair value is calcu-

lated using appropriate valuation techniques such as generally accepted option price models or

discounting future cash flows with the market interest rate, or by referring to the most recent busi-

ness transactions between knowledgeable, willing and independent business partners for one and

the same financial instrument, if necessary confirmed by the banks processing the transactions.

Amortized cost corresponds to the original cost less redemption, impairment losses and

the release of any difference between costs and the amount repayable upon maturity calculated by

applying the effective interest method. Financial instruments are recognized as soon as the Porsche

SE group becomes a party to the contractual provisions of the financial instrument. They are gener-

ally derecognized when the contractual right to the cash flows expires or this right is transferred to

a third party.