Foot Locker 2011 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2011 Foot Locker annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

Net cash used in financing activities of continuing operations was $127 million in 2010 as compared with

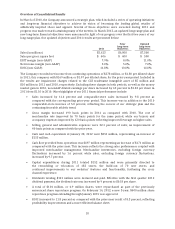

$94 million in 2009. During 2010, the Company repurchased 3,215,000 shares of its common stock for

$50 million. Additionally, the Company declared and paid dividends totaling $93 million and $94 million in

2010 and 2009, respectively, representing a quarterly rate of $0.15 per share in both 2010 and 2009.

During 2010 and 2009, the Company received proceeds from the issuance of common stock and treasury

stock in connection with the employee stock programs of $13 million and $3 million, respectively. During

2010, in connection with stock option exercises, the Company recorded excess tax benefits related to

share-based compensation of $3 million as a financing activity.

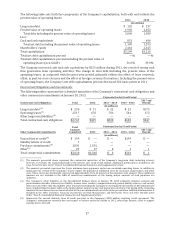

Capital Structure

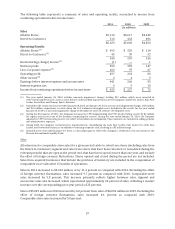

On January 27, 2012, the Company entered into an amended and restated credit agreement (the ‘‘2011

Restated Credit Agreement) with its banks, replacing the 2009 Credit Agreement. The 2011 Restated

Credit Agreement provides for a $200 million asset based revolving credit facility maturing on

January 27, 2017. In addition, during the term of the 2011 Restated Credit Agreement, the Company may

make up to four requests for additional credit commitments in an aggregate amount not to exceed $200

million. Interest is based on the LIBOR rate in effect at the time of the borrowing plus a 1.25 to 1.50

percent margin depending on certain provisions as defined in the 2011 Restated Credit Agreement.

The 2011 Restated Credit Agreement provides for a security interest in certain of the Company’s domestic

assets, including certain inventory assets, but excluding intellectual property. The Company is not required

to comply with any financial covenants as long as there are no outstanding borrowings. With regard to the

payment of dividends and share repurchases, there are no restrictions if the Company is not borrowing

and the payments are funded through cash on hand. If the Company is borrowing, Availability as of the end

of each fiscal month during the subsequent projected six fiscal months following the payment must be at

least 20 percent of the lesser of the Aggregate Commitments and the Borrowing Base (as defined in the

2011 Restated Credit Agreement). The Company’s management does not currently expect to borrow under

the facility in 2012, other than amounts used to support standby letters of credit.

Credit Rating

As of March 26, 2012, the Company’s corporate credit ratings from Standard & Poor’s and Moody’s

Investors Service are BB and Ba3, respectively. In addition, Moody’s Investors Service has rated the

Company’s senior unsecured notes B1.

Debt Capitalization and Equity (non-GAAP Measure)

For purposes of calculating debt to total capitalization, the Company includes the present value of

operating lease commitments in total net debt. Total net debt including the present value of operating

leases is considered a non-GAAP financial measure. The present value of operating leases is discounted

using various interest rates ranging from 4.25 percent to 14.5 percent, which represent the Company’s

incremental borrowing rate at inception of the lease. Operating leases are the primary financing vehicle

used to fund store expansion and, therefore, we believe that the inclusion of the present value of operating

leases in total debt is useful to our investors, credit constituencies, and rating agencies.

26