Experian 2013 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2013 Experian annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

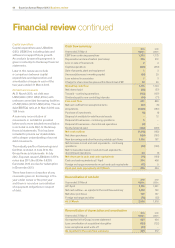

Exceptional items – continuing operations

A summary of exceptional items is given

in the table below.

As indicated in the Chief Executive’s

review, the Group launched a significant

programme of cost-efficiency measures

in November 2012. Identified efficiencies

include re-engineering fixed costs,

re-focusing resources on areas that

offer higher growth opportunities,

further near-shoring and off-shoring,

and rationalisation of products.

This programme is expected to

deliver annualised cost savings of

approximately US$75m. One-off

restructuring costs associated with

achieving these cost savings will be in the

region of US$110m, the majority of which

will be cash costs. Costs of US$54m

have been recognised in the year ended

31 March 2013 in connection with this

programme with a related cash outflow of

US$27m. Of this charge, US$41m related

to redundancy costs and US$13m related

to asset write-offs.

The loss on disposal of businesses in

the year related to a number of small

disposals of businesses.

Net interest expense

In the year ended 31 March 2013, the

net interest expense was US$58m

(2012: US$47m). The key driver of the

increase over the prior year has been

the additional funding requirement in

connection with the acquisition of the

29.6% stake in Serasa in November 2012.

Experian remains strongly cash generative

and both our interest cost and the amount

paid have continued to benefit from the

environment of low global interest rates.

There was a non-cash interest credit of

US$8m (2012: US$11m) in respect of the

difference between the expected return

on pension plan assets and interest

recognised on pension plan obligations.

Tax

The Benchmark tax rate was 25.3% (2012:

24.3%). The increase reflects increased

profits in the US and Brazil where

corporate tax rates are higher than the

main UK rate. A reconciliation of the

Benchmark tax charge is given in note 16

to the Group financial statements.

The tax charge for the year was US$152m

and the effective rate of tax for the

year was 34.5%. This is higher than the

Benchmark tax rate primarily because

the statutory profit before tax includes a

charge for the Serasa put option on which

there is no tax relief whilst there is a one-

off tax benefit on a corporate transaction

in respect of Computec. The tax credit of

US$35m in the prior year and its effective

rate of tax of (5.1%) benefited from the

determination of historic positions and

the further utilisation of tax losses.

Earnings and dividends per share

Basic earnings per share were 37.1 US cents

(2012: 66.2 US cents) including earnings per

share of 11.9 US cents (2012: loss of 0.6 US

cents) in respect of discontinued operations

(see note 19). Benchmark EPS increased to

85.7 US cents from 78.9 US cents last year.

The second interim dividend is 24.00

US cents per ordinary share (2012: 21.75

US cents) giving a total for the year of

34.75 US cents (2012: 32.00 US cents), an

increase of 9%. This is covered 2.5 times

by Benchmark EPS.

Foreign exchange

The principal exchange rates used to

translate revenue and EBIT in the year are

shown in the table at the foot of the page.

The effect of exchange rate changes on the

results for the year is to decrease reported

revenue by US$196m and EBIT by US$67m.

Cash flow and net debt commentary

Cash flow

We generated good cash flow in the year

with operating cash flow of US$1,175m

(2012: US$1,124m) and a cash flow

conversion of 94% (2012: 96%). Working

capital and capital expenditure is

managed with the aim of converting at

least 90% of EBIT into operating cash flow

and this target forms a key performance

indicator. Accordingly, our record on this

metric over a period of five years is shown

in the key performance indicators section

of this report. A reconciliation of cash

generated from operations as reported

in the Group cash flow statement to

operating cash flow as reported in the

cash flow summary table is given in note

44 to the Group financial statements.

As indicated in the cash flow summary

table overleaf, free cash flow in the year

ended 31 March 2013 was US$891m

(2012: US$889m). The net cash outflow in

the year of US$1,018m (2012: US$182m)

is after acquisition spend of US$1,549m

(2012: US$787m) and equity dividends of

US$322m (2012: US$290m). Acquisition

spend in both the current and prior years

includes significant developments for

the Group in Latin America with the

acquisition of the further stake in Serasa

in November 2012 and the acquisition of

Computec, completed in November 2011.

The analysis of acquisition spend is given

in note 44(f).

Exceptional items – continuing operations

Year ended 31 March

2013

US$m

2012

US$m

Restructuring costs 54 –

Loss/(gain) on disposal of businesses 12 (8)

Interest income on legacy tax balances –(4)

Total exceptional charge/(credit) 66 (12)

Foreign exchange – average rates

2013 2012

Weakened

against the US$

Sterling : US$ 1.58 1.60 1.2%

US$ : Brazilian real 2.01 1.70 18.2%

Euro : US$ 1.29 1.38 6.5%

P32

Business overview Business review Governance Financial statements

45