ComEd 2006 Annual Report Download - page 269

Download and view the complete annual report

Please find page 269 of the 2006 ComEd annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

278 -

279

279 -

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

|

|

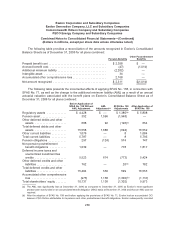

Exelon Corporation and Subsidiary Companies

Exelon Generation Company, LLC and Subsidiary Companies

Commonwealth Edison Company and Subsidiary Companies

PECO Energy Company and Subsidiary Companies

Combined Notes to Consolidated Financial Statements—(Continued)

(Dollars in millions, except per share data unless otherwise noted)

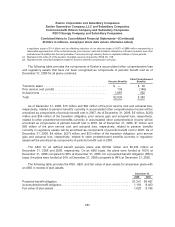

Exelon’s traditional and cash balance pension plans and AmerGen’s cash balance pension plan

are intended to be tax-qualified defined benefit plans, and Exelon submitted applications to the IRS for

rulings on the tax-qualification of the form of its plans for non-union and electing union employees. On

June 1, 2004, the IRS issued a favorable ruling on the union cash balance plan. Exelon has not yet

received a ruling with respect to its non-union plan, and AmerGen has not yet submitted an application

with respect to its cash balance formula, due to the IRS temporary moratorium on issuing any rulings to

plans that were involved in a “conversion” from a traditional to a cash balance formula. In December

2006, the IRS issued a notice announcing that the moratorium on consideration of determination letters

for cash balance plans would be lifted in 2007.

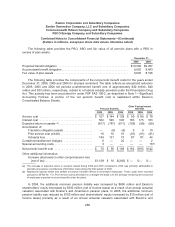

The costs of providing benefits under these plans are dependent on historical information such as

employee age, length of service and level of compensation and the actual rate of return on plan assets.

Also, Exelon and AmerGen utilize assumptions about the future, including the expected rate of return

on plan assets, the discount rate applied to benefit obligations, the incidence of mortality, the remaining

service period, rate of compensation increases and the anticipated rate of increase in health care

costs, in order to measure the plan obligations and costs to be recognized related to these plans. The

impact of changes in these factors on pension and other postretirement benefit obligations is generally

recognized over the expected remaining service life of the employees rather than immediately

recognized in the income statement. Exelon and AmerGen use a December 31 measurement date for

their plans.

Funding is based upon actuarially determined contributions that take into account the amount

deductible for income tax purposes and the minimum contribution required under ERISA, as amended.

The funded status of the pension and other postretirement benefit obligations refers to the difference

between plan assets and estimated obligations of the plan. The funded status may change over time

due to several factors, including contribution levels, assumed discount rates and actual long-term rates

of return on plan assets. Changes in these factors could impact the funded status of these obligations.

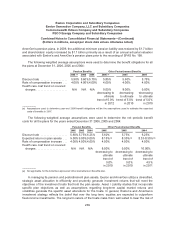

Exelon made discretionary aggregate contributions of approximately $2 billion to its traditional and

cash balance pension plans in 2005. The 2005 contributions were initially funded through borrowings

under a short-term loan agreement, which were subsequently refinanced with long-term senior notes,

as further described in Note 11—Debt and Credit Agreements.

In accordance with SFAS No. 158, which became effective in the fourth quarter of 2006, Exelon

and Generation are required to recognize the overfunded or underfunded status of their defined benefit

pension and other postretirement plans as an asset or liability on their balance sheets as of

December 31, 2006. The impacts of adopting SFAS No. 158 to Exelon’s and Generation’s

Consolidated Balance Sheets is described in more detail below.

In 2006, President Bush signed into law the Pension Protection Act of 2006 (the Act), which will

affect the manner in which many companies, including Exelon and Generation, administer their

pension plans. This legislation will require companies to, among other things, increase the amount by

which they fund their pension plans, pay higher premiums to the Pension Benefit Guaranty Corporation

if they sponsor defined benefit plans, amend plan documents and provide additional plan disclosures in

regulatory filings and to plan participants. This legislation will be effective as of January 1, 2008.

Exelon and Generation do not anticipate that the Act will have a material effect on their liquidity and

capital resources. Absent changes in plan design as a result of the Act, the Act is not expected to

264