ComEd 2006 Annual Report Download - page 207

Download and view the complete annual report

Please find page 207 of the 2006 ComEd annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

|

|

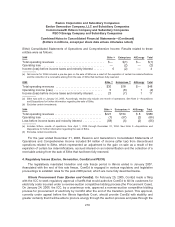

Exelon Corporation and Subsidiary Companies

Exelon Generation Company, LLC and Subsidiary Companies

Commonwealth Edison Company and Subsidiary Companies

PECO Energy Company and Subsidiary Companies

Combined Notes to Consolidated Financial Statements—(Continued)

(Dollars in millions, except per share data unless otherwise noted)

Cumulative Effect of Changes in Accounting Principles

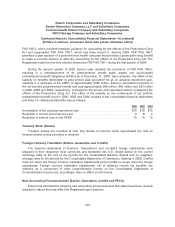

FIN 47. In March 2005, the FASB issued FIN 47, which clarifies that the term “conditional asset

retirement obligation” as used in SFAS No. 143 refers to a legal obligation to perform an asset

retirement activity in which the timing and/or method of settlement are conditional on a future event that

may or may not be within the control of the entity. FIN 47 requires an entity to recognize a liability for

the fair value of a conditional asset retirement obligation if the fair value of the liability can be

reasonably estimated. FIN 47 was effective for the Registrants as of December 31, 2005. See

Note 13—Asset Retirement Obligations for further information. The following table shows the charge

the Registrants recorded as a cumulative effect of a change in accounting principle pursuant to the

adoption of FIN 47 in 2005.

Exelon Generation ComEd PECO

Charge recorded, net of tax ................................. $42 $30 $9 $3

Related tax impact ........................................ 27 19 6 2

EITF 03-16. In March 2004, the EITF reached a consensus on and the FASB ratified EITF Issue

No. 03-16, “Accounting for Investments in Limited Liability Companies” (EITF 03-16). The EITF

concluded that if investors in a limited liability company have specific ownership accounts, they should

follow the guidance prescribed in Statement of Position 78-9, “Accounting for Investments in Real

Estate Ventures,” and EITF Topic No. D-46, “Accounting for Limited Partnership Investments.”

Otherwise, investors should follow the significant influence model prescribed in Accounting Principles

Board Opinion No. 18, “The Equity Method of Accounting for Investments in Common Stock.” EITF

03-16 was effective for Exelon and its subsidiaries during the third quarter of 2004. Exelon recorded a

charge of $9 million (net of an income tax benefit of $5 million) as a cumulative effect of a change in

accounting principle in connection with its adoption of EITF 03-16 as of July 1, 2004. This charge

related to certain investments in limited liability partnerships held by Enterprises.

FIN 46-R. See discussion of the adoption of FIN 46-R within the “Variable Interest Entities”

discussion above.

202