ComEd 2006 Annual Report Download - page 131

Download and view the complete annual report

Please find page 131 of the 2006 ComEd annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

|

|

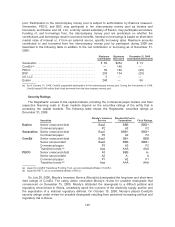

On July 31, 2006, Fitch Ratings downgraded the long-term ratings of ComEd. On November 17,

2006, Fitch Ratings placed the ratings of ComEd under Ratings Watch negative due to on-going

uncertainty in Illinois resulting from recent legislative actions supporting a rate freeze.

On October 5, 2006, Standard & Poor’s (S&P) downgraded the short-term and long-term security

ratings of ComEd due to perceived political risk related to the rate freeze extension proposal. S&P

downgraded ComEd’s senior unsecured debt to BB+, which is below investment grade. The ratings on

Exelon, PECO and Generation were affirmed. The ratings for all Registrants were placed under Credit

Watch with negative implications.

None of the Registrants’ borrowings is subject to default or prepayment as a result of a

downgrading of securities although such a downgrading could increase fees and interest charges

under the Registrants’ credit facilities.

A security rating is not a recommendation to buy, sell or hold securities and may be subject to

revision or withdrawal at any time by the assigning rating agency.

As part of the normal course of business, Generation routinely enters into physical or financially

settled contracts for the purchase and sale of capacity, energy, fuels and emissions allowances. These

contracts either contain express provisions or otherwise permit Generation and its counterparties to

demand adequate assurance of future performance when there are reasonable grounds for doing so.

In accordance with the contracts and applicable contracts law, if Exelon or Generation is downgraded

by a credit rating agency, especially if such downgrade is to a level below investment grade, it is

possible that a counterparty would attempt to rely on such a downgrade as a basis for making a

demand for adequate assurance of future performance. Depending on its net position with a

counterparty, the demand could be for the posting of collateral. In the absence of expressly agreed to

provisions that specify the collateral that must be provided, the obligation to supply the collateral

requested will be a function of the facts and circumstances of Exelon or Generation’s situation at the

time of the demand. If Exelon can reasonably claim that it is willing and financially able to perform its

obligations, it may be possible to successfully argue that no collateral should be posted or that only an

amount equal to two or three months of future payments should be sufficient.

Shelf Registrations

As of December 31, 2006, Exelon and PECO had current shelf registration statements for the sale

of $300 million and $250 million, respectively, of securities that were effective with the SEC. ComEd, a

well-known seasoned issuer as described by the SEC, filed an automatic registration statement on

May 10, 2006 and the shelf registration was effective immediately. The ability of Exelon, ComEd or

PECO to sell securities off its shelf registration statement or to access the private placement markets

will depend on a number of factors at the time of the proposed sale, including other required regulatory

approvals, the current financial condition of the company, its securities ratings and market conditions.

Regulatory Restrictions

The issuance by ComEd of long-term debt or equity securities requires the prior authorization of

the ICC. The issuance by PECO of long-term debt or equity securities requires the prior authorization

of the PAPUC. ComEd and PECO normally obtain the required approvals on a periodic basis to cover

their anticipated financing needs for a period of time or in connection with a specific financing.

Under PUHCA, the SEC had financing jurisdiction over ComEd’s and PECO’s short-term

financings and all of Generation’s and Exelon’s financings. As a result of the repeal of PUHCA,

126