ComEd 2006 Annual Report Download - page 205

Download and view the complete annual report

Please find page 205 of the 2006 ComEd annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

|

|

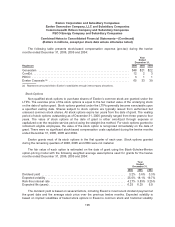

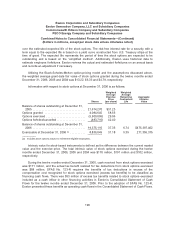

Exelon Corporation and Subsidiary Companies

Exelon Generation Company, LLC and Subsidiary Companies

Commonwealth Edison Company and Subsidiary Companies

PECO Energy Company and Subsidiary Companies

Combined Notes to Consolidated Financial Statements—(Continued)

(Dollars in millions, except per share data unless otherwise noted)

FIN 48

In June 2006, the FASB issued FIN 48, “Accounting for Uncertainty in Income Taxes, an

Interpretation of FASB Statement No. 109” (FIN 48), which clarifies the accounting for uncertainty in

income taxes recognized in accordance with SFAS No. 109, “Accounting for Income Taxes.” FIN 48

applies to all income tax positions taken on previously filed tax returns or expected to be taken on a

future tax return. FIN 48 prescribes a benefit recognition model with a two-step approach, a more-

likely-than-not recognition criterion and a measurement attribute that measures the position as the

largest amount of tax benefit that is greater than 50% likely of being ultimately realized upon ultimate

settlement. If it is not more likely than not that the benefit will be sustained on its technical merits, no

benefit will be recorded. Uncertain tax positions that relate only to timing of when an item is included on

a tax return are considered to have met the recognition threshold for purposes of applying FIN 48.

Therefore, if it can be established that the only uncertainty is when an item is taken on a tax return,

such positions have satisfied the recognition step for purposes of FIN 48 and uncertainty related to

timing should be assessed as part of measurement. FIN 48 also requires that the amount of interest

expense and income to be recognized related to uncertain tax positions be computed by applying the

applicable statutory rate of interest to the difference between the tax position recognized in accordance

with FIN 48 and the amount previously taken or expected to be taken in a tax return.

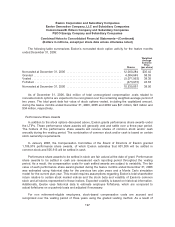

FIN 48 was effective for the Registrants as of January 1, 2007. The change in net assets as a

result of applying this pronouncement will be a change in accounting principle with the cumulative

effect of the change required to be treated as an adjustment to the opening balance of retained

earnings. Adjustments to goodwill or regulatory accounts associated with the implementation of FIN 48

will be based on other applicable accounting standards. The Registrants have not fully completed the

process of evaluating the impact of adopting FIN 48, including the apportionment of the tax and interest

impacts to the Registrants in Exelon’s affiliated group. Nevertheless, the Registrants have performed

procedures to identify a range of the anticipated impacts of the adoption of FIN 48. The adoption of FIN

48 is not anticipated to have a material impact on the Registrants’ January 1, 2007 balance of retained

earnings. The estimated impact of the adoption of FIN 48 on the Registrants’ financial statements is

subject to change due to potential changes in interpretation of FIN 48 by the FASB and other

regulatory bodies and the finalization of the Registrants’ adoption efforts.

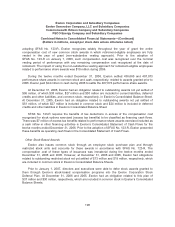

EITF 06-3

In June 2006, the FASB ratified EITF Issue No. 06-3, “How Sales Taxes Collected from

Customers and Remitted to Governmental Authorities Should Be Presented in the Income Statement

(That Is, Gross Versus Net Presentation)” (EITF 06-3). EITF 06-3 provides guidance on disclosing the

accounting policy for the income statement presentation of any tax assessed by a governmental

authority that is directly imposed on a revenue-producing transaction between a seller and a customer

on either a gross (included in revenues and costs) or a net (excluded from revenues) basis. In addition,

EITF 06-3 requires disclosure of any such taxes that are reported on a gross basis as well as the

amounts of those taxes in interim and annual financial statements for each period for which an income

statement is presented. EITF 06-3 will be effective for the Registrants as of January 1, 2007. The

200