Suzuki 2003 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2003 Suzuki annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47

|

|

SUZUKI MOTOR CORPORATION

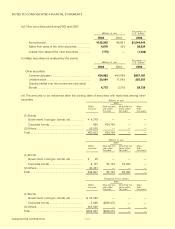

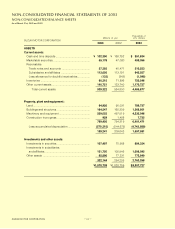

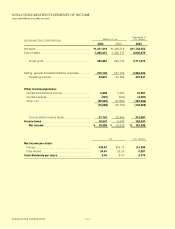

12. Contingent liabilities

As of March 31, 2003, the Company and certain consolidated subsidiaries had the following

contingent liabilities:

Millions of Thousands of

yen U.S. dollars

Guarantee of indebtedness of affiliates and others .

¥12,684 $105,531

Trade notes discounted ....................................... 1,715 14,270

¥14,400 $119,801

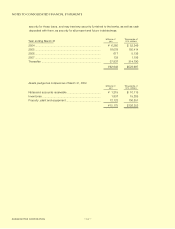

Operating lease transactions as of March 31, 2003 were as follows:

As a lessee Thousands of

Millions of yen U.S. dollars

2003 2002 2003

Future lease payments

Due within one year ..................................... ¥ 190 ¥185 $1,585

Thereafter ..................................................... 517 617 4,308

¥ 708 ¥803 $5,894

Thousands of

Millions of yen U.S. dollars

2003 2002 2003

Future lease revenues

Due within one year ..................................... ¥ 65 ¥ 32 $ 544

Thereafter ..................................................... 160 26 1,336

¥ 226 ¥ 59 $1,881

As a lessor

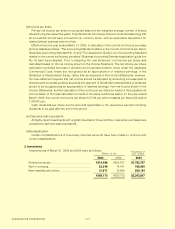

11. Shareholders' equity

The Commercial Code requires that at least 50% of the issue price of new shares be included in a

company's stated capital. The portion to be recorded as stated capital is determined by resolution of

the Board of Directors. Proceeds in excess of the stated capital should be credited to "Additional

paid-in capital".

The Commercial Code provides that an amount equivalent to a minimum of 10% of cash dividends

and bonuses paid to directors and corporate auditors should be appropriated as a legal reserve

until the reserve reaches a certain limit, defined as 25% of the stated capital less certain capital

reserves.

The Commercial Code allows both the capital reserve, including "Additional paid-in capital", and

the legal reserve to be transferred to the stated capital, by resolution of the Board of Directors, or to

be used to reduce a deficit following the approval at a shareholders' meeting. In addition, under the

Commercial Code, the capital reserve and the legal reserve may be available for dividends to the

extent that the total of the capital and legal reserve taken together do not fall below 25% of the stated

capital. The legal reserves of the Company and its subsidiaries are included in "Retained Earnings"

on the consolidated balance sheet and are not shown separately.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

38