Red Lobster 2010 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2010 Red Lobster annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

|

|

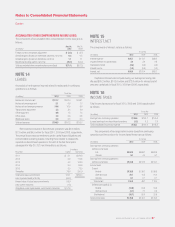

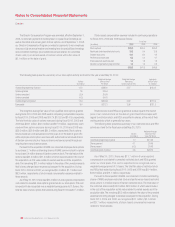

The effect of derivatives not designated as hedging instruments on the

consolidated statements of earnings for the years ended May 30, 2010 and

May 31, 2009, are as follows:

Location of Gain (Loss) Amount of Gain (Loss)

Recognized In Recognized in Income

(in millions) Income on Derivatives May 30, 2010 May 31, 2009

Commodity contracts Cost of Sales(1) $(0.2) $(5.0)

Equity forwards Cost of Sales(2) 2.2 2.1

Equity forwards Selling, General and Administrative 1.3 0.9

$ 3.3 $(2.0)

(1) Location of gain (loss) recognized in income is food and beverage costs and restaurant

expenses, which are components of cost of sales.

(2) Location of gain (loss) recognized in income is restaurant labor expenses, which is a

component of cost of sales.

Based on the fair value of our derivative instruments designated as cash

flow hedges as of May 30, 2010, we expect to reclassify $0.2 million of net

losses on derivative instruments from accumulated other comprehensive

income (loss) to earnings during the next twelve months based on the timing

of our forecasted commodity purchases and maturity of equity forward

instruments. However, the amounts ultimately realized in earnings will be

dependent on the fair value of the contracts on the settlement dates. We are

currently party to foreign currency forward contracts designated as cash flow

hedges to mitigate the risk of variability in our cash flows from fluctuations in

exchange rates specifically related to forecasted payments for services

through August 2011.

DARDEN RESTAURANTS, INC. | 2010 ANNUAL REPORT 55

Notes to Consolidated Financial Statements

Darden

NOTE 11

FAIR VALUE MEASUREMENTS

The fair values of cash equivalents, accounts receivable, accounts payable and short-term debt approximate their carrying amounts due to their short duration.

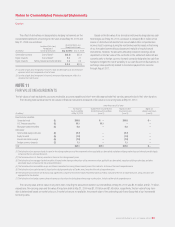

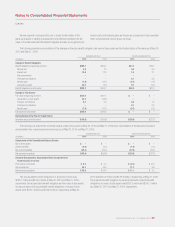

The following table summarizes the fair values of financial instruments measured at fair value on a recurring basis at May 30, 2010:

Items Measured at Fair Value

Fair Value of Quoted Prices in Active Market Significant Other Significant

Assets (Liabilities) for Identical Assets (Liabilities) Observable Inputs Unobservable Inputs

(In millions) at May 30, 2010 (Level 1) (Level 2) (Level 3)

Fixed-income securities:

Corporate bonds (1) $15.8 $ – $15.8 $ –

U.S. Treasury securities (2) 10.1 10.1 – –

Mortgage-backed securities (3) 5.8 – 5.8 –

Derivatives:

Commodities swaps & futures (4) (0.7) – (0.7) –

Equity forwards (5) (1.0) – (1.0) –

Interest rate locks & swaps (6) (7.0) – (7.0) –

Foreign currency forwards (7) 1.1 – 1.1 –

Total $24.1 $10.1 $14.0 $ –

(1) The fair value of our corporate bonds is based on the closing market prices of the investments when applicable, or, alternatively, valuations utilizing market data and other observable inputs,

inclusive of the risk of nonperformance.

(2) The fair value of our U.S. Treasury securities is based on the closing market prices.

(3) The fair value of our mortgage-backed securities is based on the closing market prices of the investments when applicable, or, alternatively, valuations utilizing market data and other

observable inputs, inclusive of the risk of nonperformance.

(4) The fair value of our commodities swaps and futures is based on the closing futures market prices of the contracts, inclusive of the risk of nonperformance.

(5) The fair value of our equity forwards is based on the closing market value of Darden stock, inclusive of the risk of nonperformance.

(6) The fair value of our interest rate lock and swap agreements is based on the present value of expected future cash flows, inclusive of the risk of nonperformance, using a discount rate

appropriate for the duration.

(7) The fair value of our foreign currency forward contracts is based on the closing forward exchange market prices, inclusive of the risk of nonperformance.

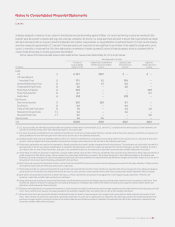

The carrying value and fair value of long-term debt, including the amounts included in current liabilities, at May 30, 2010 was $1.63 billion and $1.71 billion,

respectively. The carrying value and fair value of long-term debt at May 31, 2009 was $1.63 billion and $1.49 billion, respectively. The fair value of long-term

debt is determined based on market prices or, if market prices are not available, the present value of the underlying cash flows discounted at our incremental

borrowing rates.