Qantas 2010 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2010 Qantas annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

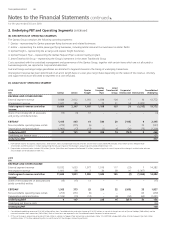

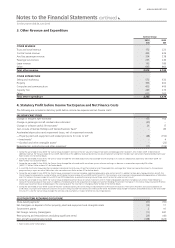

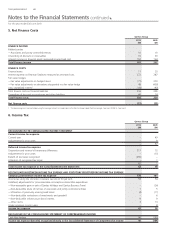

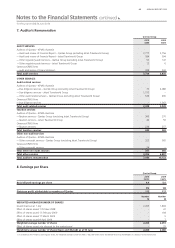

55 ANNUAL REPORT 2010

for the year ended 30 June 2010

Notes to the Financial Statements continued

(H) GOODS AND SERVICES TAX (GST)

Revenues, expenses and assets are recognised net of the amount of GST,

except where the amount of GST incurred is not recoverable from the

taxation authority. In these circumstances, the GST is recognised as part

of the cost of acquisition of the asset or as part of the expense.

Receivables and payables are stated with the amount of GST included.

The net amount of GST recoverable from, or payable to, the taxation

authority is included as a current asset or liability in the Balance Sheet.

Cash ows are included in the Consolidated Cash Flow Statement on a

gross basis. The GST components of cash ows arising from investing

and nancing activities which are recoverable from, or payable to, the

taxation authority are classi ed as operating cash ows.

(I) MAINTENANCE AND OVERHAUL COSTS

Accounting for the cost of providing major airframe and certain engine

maintenance checks for owned aircraft is described in the accounting

policy for property, plant and equipment in Note 1(P). With respect to

operating lease agreements, where the Qantas Group is required to

return the aircraft with adherence to certain maintenance conditions,

provision is made during the lease term. This provision is based on the

present value of the expected future cost of meeting the maintenance

return condition having regard to the current eet plan and long-term

maintenance schedules. The present value of non-maintenance return

conditions is provided for at the inception of the lease.

All other maintenance costs are expensed as incurred, except overhaul

costs covered by third party maintenance agreements where there is a

transfer of risk and legal obligation, which are expensed on the basis

of hours own. Modi cations that enhance the operating performance

or extend the useful lives of airframes or engines are capitalised and

depreciated over the remaining estimated useful life of the asset.

(J) INCOME TAX

Income tax expense comprises current and deferred tax. Income tax

expense is recognised in the Consolidated Income Statement except to

the extent that it relates to items recognised directly in equity or in other

comprehensive income, in which case it is recognised in equity or in

other comprehensive income.

Current tax liability is the expected tax payable on the taxable income for

the year, using tax rates enacted or substantially enacted at balance date

and any adjustment to tax payable with respect to previous years.

Deferred tax is recognised in respect of temporary differences between

the carrying amounts of assets and liabilities for nancial reporting

purposes and the amounts used for taxation purposes. Deferred tax is not

recognised for temporary differences arising from the initial recognition

of assets or liabilities that affect neither accounting nor taxable pro t,

and differences relating to investments in controlled entities and

associates and jointly controlled entities to the extent that they will

probably not reverse in the foreseeable future. In addition, deferred tax

is not recognised for taxable temporary differences arising on the initial

recognition of goodwill. The amount of deferred tax provided is based

on the expected manner of realisation or settlement of the carrying

amount of assets and liabilities, using tax rates enacted or substantially

enacted at balance date.

A deferred tax asset is recognised only to the extent that it is probable

that future taxable pro ts will be available against which the asset can

be utilised. Deferred tax assets are reduced to the extent that it is no

longer probable that the related tax bene t will be realised.

Qantas provides for income tax in both Australia and overseas

jurisdictions where a liability exists.

(K) TAX CONSOLIDATION

Qantas and its Australian wholly-owned controlled entities and partnerships

are part of a tax consolidated group. As a consequence, all members of the

tax consolidated group are taxed as a single entity.

(L) RECEIVABLES

Current receivables are recognised and carried at original invoice amount

less impairment losses. Bad debts are written off as incurred. Non-current

receivables are carried at the present value of future net cash in ows

expected to be received.

(M) CONTRACT WORK IN PROGRESS

Contract work in progress is stated at cost plus pro t recognised to date,

in accordance with Note 1(G), less an allowance for foreseeable losses

and less progress billings. Cost includes all expenditure related directly

to speci c projects and an allocation of xed and variable overheads

incurred in the Qantas Group’s contract activities based on normal

operating capacity.

Contract work in progress is presented as part of trade and other

receivables in the Consolidated Balance Sheet. If payments received

from customers exceed the income recognised, then the difference is

presented as deferred income in the Consolidated Balance Sheet.

(N) INVENTORIES

Inventories are measured at the lower of cost and net realisable value.

The costs of engineering expendables, consumable stores and work in

progress are assigned to the individual items of inventories on the basis

of weighted average costs.

(O) IMPAIRMENT

Non- nancial Assets

The carrying amounts of non- nancial assets (other than inventories and

deferred tax assets) are reviewed at each balance date to determine

whether there is any indication of impairment. If any such indication

exists, the assets’ recoverable amount is estimated. For goodwill and

intangible assets with inde nite lives, the recoverable amount is

estimated each year.

The recoverable amount of assets is the greater of their fair value less

costs to sell and value in use. Assets which primarily generate cash ows

as a group, such as aircraft, are assessed on a cash generating unit

(CGU) basis inclusive of related infrastructure and intangible assets and

compared to net cash ows for the CGU. Estimated net cash ows

used in determining recoverable amounts are discounted to their net

present value using a pre-tax discount rate that re ects current market

assessments of the time value of money and the risks speci c to the asset.

An appropriate impairment charge is made if the carrying amount of

an asset or CGU exceeds its recoverable amount. The impairment is

expensed in the year in which it occurs. An impairment loss is reversed if

there has been a change in the estimates used to determine the

recoverable amount. An impairment loss with respect to goodwill is not

reversed.

Financial Assets

The carrying value of nancial assets is assessed at each reporting date

to determine whether there is any objective evidence that it is impaired.

A nancial asset is considered to be impaired if objective evidence

indicates that one or more events have had a negative effect on the

estimated future cash ows of that asset.

An impairment loss in respect of a nancial asset measured at amortised

cost is calculated as the difference between its carrying amount and the

present value of the estimated future cash ows discounted at the asset’s

original effective interest rate.

1. Statement of Signi cant Accounting Policies continued