Nissan 2012 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2012 Nissan annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42

|

|

loan authorization is made in a comprehensive manner by considering the following points: applicant’s

credit history; applicant’s capacity to pay which is estimated by debt ratio, payment to income ratio and

disposable income; applicant’s stability; and loan conditions, including the loan collateral, loan advance

and payment terms. In addition to carrying out this screening process, Nissan takes into account

qualitative information by conducting field visits to customers or referring to past business records with

Nissan, in accordance with characteristics of regional business practices and risks.

Dealer finance for inventory vehicles is authorized on the basis of an internal rating system that

takes into account the financial position of dealers, and, if necessary, personal guarantees and/or

mortgage collateral are taken in pledge in addition to inventory vehicle collaterals. These scoring

models are regularly reviewed and revised to keep them current with actual practice.

In some regions and products, Nissan also offers different pricing depending on the applicant’s

credit score to compensate the risks.

As a matter of accounting policy, Nissan maintains an allowance for doubtful accounts and credit

losses adequately to cover probable losses. Nissan makes a best effort to recover the actual losses

from bad debt accounts as quickly as possible by taking necessary actions, including flexible and

effective organization changes for collection and utilization of third-party collection services.

Residual value risks

Vehicles on operating leases and some balloon type credits, where Nissan is the lessor, are

guaranteed end-of-term residual value by Nissan. Nissan is therefore exposed to the risks that sales

value of the vehicle could fall below its contractual residual values when the financed vehicle is

returned and sold in the used car market at the end of the contract term.

To mitigate the risks mentioned above, Nissan objectively sets contractual residual value by using the

future end-of-term market value estimation by a third party such as Automotive Lease Guide in North

America, and the estimation from statistical analysis with historical data of the used car market in Japan.

To support used car market value, Nissan takes several strategic initiatives, including control of

sales incentives for new car sales promotion, fleet sales volume control and introduction of the

Certified Pre-owned program.

As a matter of accounting policy, Nissan evaluates the recoverability of carrying values of its

vehicles for impairment on an ongoing basis. If impaired, Nissan recognizes allowance for potential

residual value losses in a timely and adequate manner.

4) Counterparty

Nissan has a certain amount of exposures to counterparties in making financial transactions, such as

bank deposits, investments and derivative contracts. While we work with competitive banking

counterparties, Nissan manages its counterparty risk by using a certain evaluation system.

The evaluation system which Nissan uses is based on ratings of counterparties’ long-term credit

and financial strength, and the level of their shareholders’ equity. The system is applied to Nissan as a

group, and we set limits in terms of amount and term on a consolidated basis. By making the analysis

monthly, we are able to take action on a timely basis when any concerns arise.

5) Pension

Nissan has defined benefit pension plans mainly in Japan, the United States and the United Kingdom.

Funding policy for pension plans is to make periodic contributions as required by applicable

regulations. Benefit obligations and pension costs are calculated using many different drivers, such as

discount rate and rate of salary/wage increase.

Plan assets are exposed to financial market risks as they are invested in various types of financial

assets including bonds and stocks. When the fair value of these assets declines, the amount of the

unfunded portion of pension plans increases, which could materially affect cash-out and costs for

Nissan in the form of future contribution to the pension plans.

As countermeasures to manage such risks, the investment policy of these pension plans is based

upon the liability profile of the plans, long term investment views and benchmark information regarding

asset allocation of other corporate pension plans.

In addition, Nissan convenes Global Pension Committees on a periodic basis to review investment

performance, manager performance, review asset allocations and discuss other issues related to

pension assets.

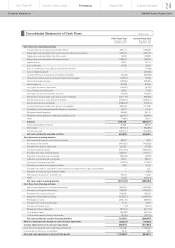

Innovation & Power of brandYear 2 Power 88 Performance Corporate Data

Corporate Governance 32

NISSAN Annual Report 2012Maintaining Trust Through Transparency