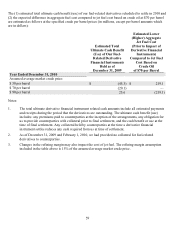

Airtran 2009 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2009 Airtran annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

55

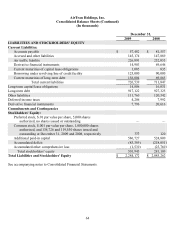

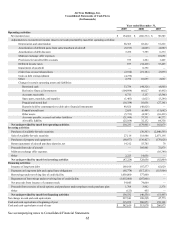

derivative. The Cash Conversion Topic required retroactive application to all periods presented. The adoption

impacted the accounting for our 7.0% convertible notes due 2023. On April 24, 2009, we filed a report on Form

8-K with the SEC which included our consolidated financial statements as of December 31, 2008 and 2007 and

for each of the three years in the period ended December 31, 2008 which were adjusted to apply the Cash

Conversion Topic retroactively. The accompanying historical financial statements have also been adjusted to

apply the Cash Conversion Topic.

On June 30, 2009, we adopted ASC 855-10-50 “Subsequent Events - Disclosure” (Subsequent Events Topic),

which established general standards of accounting for, and disclosure of, events that occur after the balance

sheet date but before the financial statements are issued.The Subsequent Events Topic defines two types of

subsequent events. The effects of events or transactions that provide additional evidence about conditions that

existed at the balance sheet date, including the estimates inherent in the process of preparing financial

statements, are recognized in the financial statements. The effects of events that provide evidence about

conditions that did not exist at the date of the balance sheet but arose after that date are not recognized in the

financial statements. We have reviewed subsequent events through February 11, 2010 (the date of the issuance

of the accompanying Consolidated Financial Statements).