Air New Zealand 2012 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 2012 Air New Zealand annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

AIR NEW ZEALAND ANNUAL FINANCIAL RESULTS 2012

14

present value. Aircraft which have been withdrawn from service and have no intention of being reintroduced into the operating fleet are

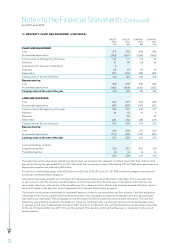

assessed for impairment on an individual basis.

Where an impairment loss subsequently reverses, the carrying amount of the asset or cash-generating unit is increased to the revised

estimate of its recoverable amount, but so that the increased carrying amount does not exceed the carrying amount that would have

been determined had no impairment loss been recognised in prior years.

ASSETS HELD FOR RESALE

Non-current assets are classified as held for resale if their carrying amount will be recovered through a sale transaction rather

than through continuing use. The sale must be highly probable and the asset available for immediate sale in its present condition.

Management must be committed to the sale, which should be expected to qualify for recognition as a completed sale within one year

from the date of classification.

Non-current assets classified as held for resale are measured at the lower of the asset’s previous carrying amount and its fair value less

costs to sell.

WORK IN PROGRESS

Contract work in progress is stated at cost plus the profit recognised to date, using the percentage of completion method, less any

amounts invoiced to customers. Cost includes all expenses directly related to specific contracts and an allocation of direct production

overhead expenses incurred.

Capital work in progress includes the cost of materials, services, labour and direct production overheads.

INVENTORIES

Inventories are measured at the lower of cost and net realisable value. Cost is determined using the first-in, first-out (FIFO) cost method.

Net realisable value is the estimated selling price in the ordinary course of business, less applicable variable selling expenses.

SHARE CAPITAL

Ordinary shares are classified as equity. Incremental costs directly attributable to the issue of new shares or options are shown in equity

as a deduction, net of taxation, from the proceeds.

Where a member of the Group purchases the Company’s share capital, the consideration paid is deducted from equity under the

treasury stock method, until they are reissued or otherwise disposed of.

RESERVES

Cash flow hedge reserve

The cash flow hedge reserve comprises the effective portion of the cumulative net change in the fair value of cash flow hedging

instruments related to hedged transactions that have not yet occurred.

Foreign currency translation reserve

The foreign currency translation reserve comprises foreign exchange differences arising on consolidation of foreign operations together

with the translation of foreign currency borrowings designated as a hedge of net investments in those foreign operations.

Investment revaluation reserve

The investment revaluation reserve comprises changes in the fair value of the investment in quoted equity instruments.

FINANCIAL GUARANTEE CONTRACTS

Where the Company enters into financial guarantee contracts to guarantee the indebtedness of other companies within the Group, the

Company considers these to be insurance contracts (as defined by NZ IFRS 4 - Insurance contracts) and accounts for them as such.

TAXATION

The income taxation expense for the period is the taxation payable on the current period’s taxable income at tax rates enacted or

substantively enacted at reporting date. This is adjusted by changes in deferred taxation assets and liabilities. Income taxation expense

is recognised in the Statement of Financial Performance except where it relates to items recognised directly in equity, in which case it is

recognised in equity.

Deferred income taxation is provided in full, using the balance sheet liability method, on temporary differences arising between the

tax bases of assets and liabilities and their carrying amounts in the financial statements. Deferred income tax is determined using tax

rates (and laws) that have been enacted or substantively enacted by the balance sheet date and are expected to apply when the related

deferred income tax asset is realised or the deferred income tax liability is settled.

Deferred income tax assets and unused tax losses are only recognised to the extent that it is probable that future taxable amounts will

be available against which to utilise those temporary differences and losses.

Statement of Accounting Policies (Continued)

For the year to 30 June 2012