3M 2013 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2013 3M annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

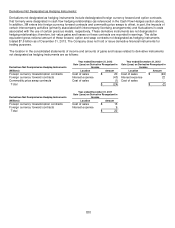

98

marked to a value with respect to changes in spot foreign currency exchange rates and not with respect to other factors

that may impact fair value.

3M has determined that foreign currency forwards and commodity price swaps will be considered level 1 measurements

as these are traded in active markets which have identical asset or liabilities, while currency swaps, foreign currency

options, interest rate swaps and cross-currency swaps will be considered level 2. For level 2 derivatives, 3M uses inputs

other than quoted prices that are observable for the asset. These inputs include foreign currency exchange rates,

volatilities, and interest rates. The level 2 derivative positions are primarily valued using standard calculations/models that

use as their basis readily observable market parameters. Industry standard data providers are 3M’s primary source for

forward and spot rate information for both interest rates and currency rates, with resulting valuations periodically validated

through third-party or counterparty quotes and a net present value stream of cash flows model.

The following tables provide information by level for assets and liabilities that are measured at fair value on a recurring

basis.

Fair Value Measurements

(Millions) Fair Value at Using Inputs Considered as

Description

Dec. 31, 2013

Level 1

Level 2

Level 3

Assets:

Available-for-sale:

Marketable securities:

U.S. government agency securities $

234

$

―

$

234

$

―

Foreign government agency securities 125

―

125

―

Corporate debt securities 781

―

781

―

Certificates of deposit/time deposits 40

―

40

―

Commercial paper 60

―

60

―

Asset-backed securities:

Automobile loan related 585

―

585

―

Credit card related 180

―

180

―

Equipment lease related 67

―

67

―

Other 75

―

75

―

U.S. treasury securities 49

49

―

―

U.S. municipal securities 2

―

2

―

Auction rate securities 11

―

―

11

Investments 2

2

―

―

Derivative instruments — assets:

Foreign currency forward/option contracts 75

75

―

―

Commodity price swap contracts 1

1

―

―

Interest rate swap contracts 8

―

8

―

Liabilities:

Derivative instruments — liabilities:

Foreign currency forward/option contracts 103

103

―

―

Interest rate swap contracts 7

―

7

―