Washington Post 2001 Annual Report Download - page 7

Download and view the complete annual report

Please find page 7 of the 2001 Washington Post annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

|

|

34

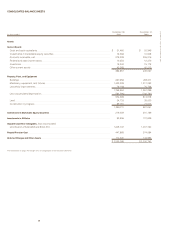

THE WASHINGTON POST COMPANY

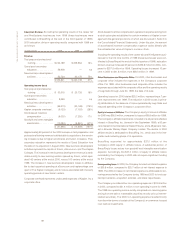

Income Taxes. The effective tax rate in 2000 was 40.6 percent, com-

pared to 39.9 percent in 1999. The increase in the effective tax rate is

principally due to the non-recognition of benefits from state net oper-

ating loss carryforwards generated by certain of the Company’s new

business start-up activities and an increase in goodwill amortization

expense that is not deductible for income tax purposes.

FINANCIAL CONDITION: CAPITAL RESOURCES AND LIQUIDITY

Acquisitions, Exchanges, and Dispositions. During 2001, the Company

spent approximately $104.4 million on business acquisitions and

exchanges, which principally included the purchase of Southern

Maryland Newspapers, a division of Chesapeake Publishing Corporation,

and amounts paid as part of a cable system exchange with AT&T

Broadband. During 2001, the Company also acquired a provider of CFA

exam preparation services and a company that provides pre-certification

training for real estate, insurance, and securities professionals.

Southern Maryland Newspapers publishes the Maryland

Independent in Charles County, Maryland; The Enterprise in

St. Mary’s County, Maryland; and The Calvert Recorder in Calvert

County, Maryland, with a combined total paid circulation of

approximately 50,000.

The cable system exchange with AT&T Broadband was completed on

March 1, 2001 and consisted of the exchange by the Company of its

cable systems in Modesto and Santa Rosa, California, and approxi-

mately $42.0 million to AT&T Broadband for cable systems serving

approximately 155,000 subscribers principally located in Idaho. In a

related transaction on January 11, 2001, the Company completed the

sale of a cable system serving about 15,000 subscribers in Greenwood,

Indiana, for $61.9 million. The gain resulting from the cable system sale

and exchange transactions increased net income by $196.5 million, or

$20.69 per share. For income tax purposes, substantial components of

the cable system sale and exchange transactions qualify as like-kind

exchanges, and therefore, a large portion of these transactions does not

result in a current tax liability.

During 2000, the Company spent $212.3 million on business

acquisitions. These acquisitions included $177.7 million for Quest

Education Corporation, a provider of post-secondary education; $16.2

million for two cable systems serving 8,500 subscribers; and $18.4 mil-

lion for various other small businesses (principally consisting of edu-

cational services companies). There were no significant business

dispositions in 2000.

During 1999, the Company acquired various businesses for about

$90.5 million, which included, among others, $18.3 million for cable

systems serving approximately 10,300 subscribers and $61.8 million

for various educational and training companies to expand Kaplan,

Inc.’s business offerings.

The Company sold the assets of Legi-Slate, Inc. in June 1999; no

significant gain or loss resulted.

Capital Expenditures. During 2001, the Company’s capital expen-

ditures totaled $224.2 million, more than half of which related to

the Company’s rollout of digital and cable modem services. The

Company’s capital expenditures for 2001, 2000, and 1999 are

itemized by operating division in Note L to the Consolidated

Financial Statements.

The Company estimates that in 2002 its capital expenditures will

decrease to approximately $130 million, as the Company’s rollout

of digital and cable modem service was nearing completion by the

end of 2001.

Investments in Marketable Equity Securities. At December 30, 2001, the

fair value of the Company’s investments in marketable equity securi-

ties was $235.4 million, which includes $219.0 million in Berkshire

Hathaway Inc. Class A and B common stock and $16.4 million of var-

ious common stocks of publicly traded companies with e-commerce

business concentrations.

At December 30, 2001, the gross unrealized gain related to the

Company’s Berkshire Hathaway Inc. stock investment totaled $34.1

million; the gross unrealized gain on this investment was $25.3 mil-

lion at December 31, 2000. The Company presently intends to hold

the Berkshire Hathaway stock long term.

Cost Method Investments. At December 30, 2001 and December 31,

2000, the Company held minority investments in various non-public

companies. The companies represented by these investments have

products or services that in most cases have potential strategic rele-

vance to the Company’s operating units. The Company records its

investment in these companies at the lower of cost or estimated fair

value. During 2001 and 2000, the Company invested $11.7 million and

$42.5 million, respectively, in various cost method investees. At

December 30, 2001 and December 31, 2000, the carrying value of the

Company’s cost method investments totaled $29.6 million and $48.6

million, respectively.

Common Stock Repurchases and Dividend Rate. During 2001, 2000, and

1999, the Company repurchased 714, 200, and 744,095 shares,

respectively, of its Class B common stock at a cost of $0.4 million, $0.1

million, and $425.9 million. The annual dividend rate for 2002 was

authorized to remain at $5.60 per share, consistent with 2001, as com-

pared to $5.40 per share in 2000, and $5.20 per share in 1999.

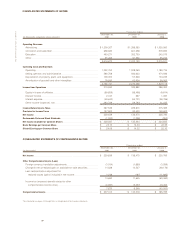

Liquidity. At December 30, 2001, the Company had $31.5 million in

cash and cash equivalents.

At December 30, 2001, the Company had $533.9 million in commer-

cial paper borrowings outstanding at an average interest rate of 2.0

percent with various maturities throughout the first and second quar-

ters of 2002. In addition, the Company had outstanding $398.1 mil-

lion of 5.5 percent, 10-year unsecured notes due February 2009.

These notes require semi-annual interest payments of $11.0 million

payable on February 15 and August 15. The Company also had $1.0

million in other debt.