Washington Post 2001 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2001 Washington Post annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

|

|

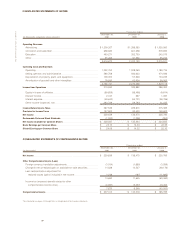

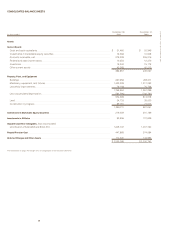

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

42

THE WASHINGTON POST COMPANY

ASUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The Washington Post Company (the “Company”) is a diversified

media organization whose principal operations consist of newspa-

per publishing (primarily The Washington Post newspaper), televi-

sion broadcasting (through the ownership and operation of six

network-affiliated television stations), the ownership and operation

of cable television systems, and magazine publishing (primarily

Newsweek magazine). Through its subsidiary Kaplan, Inc., the

Company provides educational services for individuals, schools, and

businesses. The Company also owns and operates a number of

media web sites for the primary purpose of developing the

Company’s newspaper and magazine publishing businesses on the

World Wide Web.

Fiscal Year. The Company reports on a 52–53 week fiscal year end-

ing on the Sunday nearest December 31. The fiscal years 2001,

2000, and 1999, which ended on December 30, 2001, December 31,

2000, and January 2, 2000, respectively, included 52 weeks. With

the exception of the newspaper publishing operations, subsidiaries

of the Company report on a calendar-year basis.

Principles of Consolidation. The accompanying financial statements

include the accounts of the Company and its subsidiaries; significant

intercompany transactions have been eliminated.

Presentation. Certain amounts in previously issued financial state-

ments have been reclassified to conform to the 2001 presentation.

Use of Estimates. The preparation of financial statements in con-

formity with generally accepted accounting principles requires man-

agement to make estimates and assumptions that affect the amounts

reported in the financial statements. Actual results could differ from

those estimates.

Cash Equivalents. Short-term investments with original maturities of

90 days or less are considered cash equivalents.

Investments in Marketable Equity Securities. The Company’s invest-

ments in marketable equity securities are classified as available-for-

sale and therefore are recorded at fair value in the Consolidated

Balance Sheets, with the change in fair value during the period

excluded from earnings and recorded net of tax as a separate com-

ponent of comprehensive income. Marketable equity securities that

the Company expects to hold long-term are classified as non-cur-

rent assets.

Inventories. Inventories are valued at the lower of cost or market.

Cost of newsprint is determined by the first-in, first-out method, and

cost of magazine paper is determined by the specific-cost method.

Property, Plant, and Equipment. Property, plant, and equipment is

recorded at cost and includes interest capitalized in connection with

major long-term construction projects. Replacements and major

improvements are capitalized; maintenance and repairs are charged

to operations as incurred.

Depreciation is calculated using the straight-line method over the

estimated useful lives of the property, plant, and equipment: 3 to 20

years for machinery and equipment, and 20 to 50 years for build-

ings. The costs of leasehold improvements are amortized over the

lesser of the useful lives or the terms of the respective leases.

Investments in Affiliates. The Company uses the equity method of

accounting for its investments in and earnings or losses of affiliates that

it does not control but over which it does exert significant influence.

Cost Method Investments. The Company uses the cost method of

accounting for its minority investments in non-public companies

where it does not have significant influence over the operations and

management of the investee. Investments are recorded at the lower

of cost or fair value as estimated by management. Charges recorded

to write-down cost method investments to estimated fair value and

gross realized gains or losses upon the sale of cost method invest-

ments are included in “Other income (expense), net” in the

Consolidated Statements of Income.

Goodwill and Other Intangibles. Goodwill and other intangibles rep-

resent the unamortized excess of the cost of acquiring subsidiary

companies over the fair values of such companies’ net tangible

assets at the dates of acquisition. Goodwill and other intangibles

are being amortized by use of the straight-line method over peri-

ods ranging from 15 to 40 years (with the majority being amortized

over 15 to 25 years). See New Accounting Pronouncements below

for additional discussion.

Long-lived Assets. The recoverability of long-lived assets, including

goodwill and other intangibles, is assessed whenever adverse

events and changes in circumstances indicate that previously antic-

ipated undiscounted cash flows warrant assessment.

Program Rights. The broadcast subsidiaries are parties to agree-

ments that entitle them to show syndicated and other programs on

television. The costs of such program rights are recorded when the

programs are available for broadcasting, and such costs are charged

to operations as the programming is aired.