Under Armour 2008 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2008 Under Armour annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

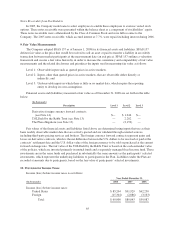

In September 2006, the FASB issued SFAS No. 157, Fair Value Measurements (“SFAS 157”), which

defines fair value, establishes a framework for measuring fair value in accordance with generally accepted

accounting principles and expands disclosures about fair value measurements. SFAS 157 was effective for fiscal

years beginning after November 15, 2007, however the FASB has delayed the effective date of SFAS 157 to

fiscal years beginning after November 15, 2008 for nonfinancial assets and nonfinancial liabilities, except those

items recognized or disclosed at fair value on an annual or more frequent basis. The adoption of SFAS 157 for

financial assets and liabilities in the first quarter of 2008 did not have a material impact on the Company’s

consolidated financial statements. The Company does not believe that the adoption of SFAS 157 for nonfinancial

assets and nonfinancial liabilities will have a material impact on its consolidated financial statements.

Recently Issued Accounting Standards

In June 2008, the FASB issued FASB Staff Position (“FSP”) Emerging Issues Task Force (“EITF”) Issue

No. 03-6-1, Determining Whether Instruments Granted in Share-Based Payment Transactions are Participating

Securities (“FSP EITF 03-6-1”). FSP EITF 03-6-1 requires that unvested stock-based compensation awards that

contain non-forfeitable rights to dividends or dividend equivalents (whether paid or unpaid) should be classified

as participating securities and should be included in the computation of earnings per share pursuant to the

two-class method as described by SFAS No. 128, Earnings per Share. The provisions of FSP EITF 03-6-1 are

required for fiscal years beginning after December 15, 2008. The Company does not believe the adoption of FSP

EITF 03-6-1 will have a material impact on its computation of earnings per share.

In June 2008, the FASB issued EITF Issue No. 07-5, Determining Whether an Instrument (or an Embedded

Feature) is Indexed to an Entity’s Own Stock (“EITF 07-5”). EITF 07-5 addresses the determination of whether

provisions that introduce adjustment features (including contingent adjustment features) would prevent treating a

derivative contract or an embedded derivative on a company’s own stock as indexed solely to the company’s

stock. EITF 07-5 is effective for fiscal years beginning after December 15, 2008. The Company does not believe

the adoption of EITF 07-5 will have a material impact on its consolidated financial statements.

In March 2008, the FASB issued SFAS No. 161, Disclosures about Derivative Instruments and Hedging

Activities (“SFAS 161”). SFAS 161 is intended to improve financial reporting about derivative instruments and

hedging activities by requiring enhanced disclosures to enable investors to better understand their effects on an

entity’s financial position, financial performance, and cash flows. The provisions of SFAS 161 are effective for

the fiscal years and interim periods beginning after November 15, 2008. The Company does not believe the

adoption of SFAS 161 will have a material impact on its consolidated financial statement disclosures.

In December 2007, the FASB issued SFAS No. 141R, Business Combinations (revised 2007) (“SFAS

141R”). SFAS 141R replaces SFAS 141 and requires the acquirer of a business to recognize and measure the

identifiable assets acquired, the liabilities assumed, and any non-controlling interest in the acquiree at fair value.

SFAS 141R also requires transaction costs related to the business combination to be expensed as incurred. SFAS

141R is effective for business combinations for which the acquisition date is on or after fiscal years beginning

after December 15, 2008. The Company does not believe the adoption of SFAS 141R will have a material impact

on its consolidated financial statements.

In December 2007, the FASB issued SFAS No. 160, Noncontrolling Interests in Consolidated Financial

Statements-an amendment of ARB No. 51 (“SFAS 160”). SFAS 160 establishes accounting and reporting

standards for the noncontrolling interest in a subsidiary and for the deconsolidation of a subsidiary. SFAS 160 is

effective for fiscal years beginning after December 15, 2008. The Company does not believe the adoption of

SFAS 160 will have a material impact on its consolidated financial statements.

59