Pfizer 2008 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2008 Pfizer annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

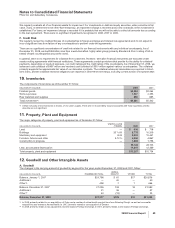

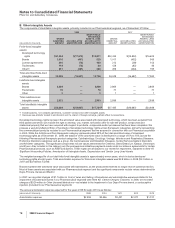

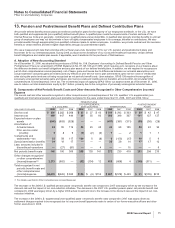

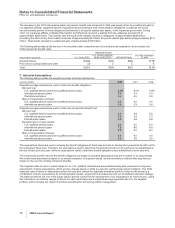

Notes to Consolidated Financial Statements

Pfizer Inc and Subsidiary Companies

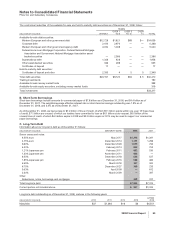

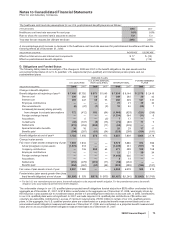

Any ineffectiveness in a hedging relationship is recognized immediately into earnings. There was no significant ineffectiveness in

2008, 2007 or 2006.

Interest Rate Risk—Our interest-bearing investments, loans and borrowings are subject to interest rate risk. We invest, loan and

borrow primarily on a short-term or variable-rate basis. From time to time, depending on market conditions, we will fix interest rates

either through entering into fixed-rate investments and borrowings or through the use of derivative financial instruments.

We entered into derivative financial instruments to hedge or offset the fixed interest rates on the hedged item, matching the amount

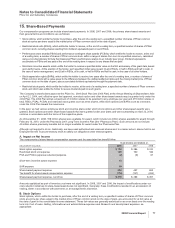

and timing of the hedged item. As of December 31, 2008 and 2007, the more significant derivative financial instruments employed to

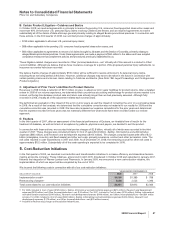

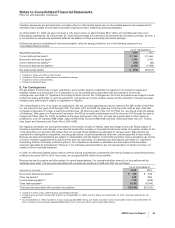

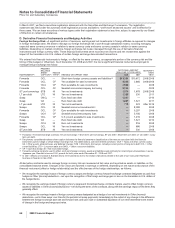

manage interest rate risk follow:

INSTRUMENT

PRIMARY

BALANCE SHEET

CAPTION(a)

HEDGE

TYPE(b) HEDGED OR OFFSET ITEM

NOTIONAL AMOUNT

(MILLIONS OF DOLLARS) MATURITY

DATE2008 2007

Swaps OA — U.S. dollar fixed rate debt $1,271 $1,278 2018-2028

Swap OA FV Euro fixed rate debt(c) 1,247 — 2014

Swap OA FV Euro fixed rate debt(c) 1,247 — 2017

Swaps OA FV U.S. dollar fixed rate debt(c) 1,050 1,050 2014-2018

Swaps OCA FV U.S. dollar fixed rate debt(c) 900 — 2009

Swap ONCL FV Euro fixed rate debt(c) —1,321 2014

Swap ONCL FV Euro fixed rate debt(c) —1,321 2017

Swaps ONCL FV U.S. dollar fixed rate debt(c) —900 2009

Swaps OCL FV U.S. dollar fixed rate debt(c) —450 2008

(a) The primary consolidated balance sheet caption indicates the financial statement classification of the fair value amount associated with the financial

instrument used to hedge or offset interest rate risk. The abbreviations used are defined as follows: OCA = Taxes and other current assets; OCL =

Other current liabilities; ONCL = Other noncurrent liabilities; and OA = Other assets, deferred taxes and deferred charges.

(b) FV = Fair value hedge.

(c) Serve to reduce exposure to long-term U.S. dollar and euro interest rates by effectively converting fixed rates associated with long-term debt

obligations to floating rates (see also Note 9C. Financial Instruments: Long-Term Debt).

All derivative contracts used to manage interest rate risk are measured at fair value and reported as assets or liabilities on the

consolidated balance sheet. Changes in fair value are reported in earnings, as follows:

•We recognize the earnings impact of interest rate swaps designated as fair value hedges in Other (income)/deductions—net upon the

recognition of the change in fair value of the hedged risk.

•We recognize the earnings impact of interest rate swaps that serve as offsets immediately in Other (income)/deductions—net.

Any ineffectiveness in a hedging relationship is recognized immediately in earnings. There was no significant ineffectiveness in

2008, 2007 or 2006.

2008 Financial Report 67