Office Depot 2001 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2001 Office Depot annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

|

|

27

Interbank Offered Rate (“TIBOR”). These facilities are available to us until

July 2002, and are therefore classified as current on our balance sheet. The

yen facilities loan agreements are tied to the covenants in our domestic facil-

ities described earlier. As of December 29, 2001, we had outstanding yen

borrowings equivalent to $74.5 million under these yen facilities, with an

average effective interest rate of 1.118%. Effective October 28, 1999, we

entered into a yen interest rate swap with a financial institution for a princi-

pal amount equivalent to $18.6 million at December 29, 2001 in order to

hedge against the volatility of the interest payments on a portion of our yen

borrowings. The terms of the swap specify that we pay an interest rate of

0.700% and receive TIBOR. The swap will mature in July 2002.

In addition to bank borrowings, we have historically used equity capital,

convertible debt and capital equipment leases as supplemental sources of funds.

In October 2001, our Board of Directors authorized the Company to

repurchase up to $50 million of its common stock each year until rescinded

by the Board. The repurchased shares will be added to the Company’s treasury

shares and will be used to meet the Company’s near-term requirements for

its stock option and other benefit plans. During 2001, we repurchased

approximately 252,000 shares of our stock at a total cost of $4.2 million

plus commissions.

In August 1999, our Board approved a $500 million stock repurchase

program reflecting its belief that our common stock represented a significant

value at its then-current trading price. We purchased 46.7 million shares of

our stock at a total cost of $500 million plus commissions during the third

and fourth quarters of 1999. During the first half of 2000, our Board approved

additional stock repurchases of up to $300 million, bringing our total author-

ization to $800 million. We completed these programs during 2000, purchasing

an additional 35.4 million shares of our stock at a total cost of $300 million

plus commissions.

In 1992 and 1993, we issued certain Liquid Yield Option Notes (“LYONst”),

which are zero coupon, convertible subordinated notes maturing in 2007

and 2008, respectively. Each LYONtis convertible at the option of the holder

at any time on or prior to its maturity into Office Depot common stock at

conversion rates of 43.895 and 31.851 shares per 1992 and 1993 LYONt,

respectively. On November 1, 2000, the majority of the holders of our 1993

LYONstrequired us to purchase the LYONstfrom them at the issue price

plus accrued original issue discount. We paid the holders $249.2 million in

connection with this repurchase, and reclassified the remaining 1993 LYONst

obligation as long-term. Our 1992 LYONsthave a similar provision whereby

the holders may require us to purchase these notes at the issue price plus

accrued original issue discount on December 11, 2002, and therefore, these

obligations totaling $233.5 million have been classified as a current liability

on our Consolidated Balance Sheet. If the holders decide to exercise their put

option, we have the choice of paying the holders in cash, common stock or

a combination of the two.

Our 2001 net cash used in financing activities consisted mainly of long-

and short-term debt payments of $400.5 million to pay off our domestic credit

facility debt that was accumulated in the fourth quarter of 2000. These pay-

ments were partially offset by proceeds received in 2001 from the issuance of

$250 million in senior subordinated notes as discussed above. For 2000, our

stock repurchase and the repurchase of our 1993 LYONstmade up the major-

ity of cash used in financing activities. We began borrowing from our domestic

credit facilities during the fourth quarter of 2000, primarily to fund the

LYONstrepurchase. We continually review our financing options. Although

we currently anticipate that we will finance all of our 2002 operations, expan-

sion and other activities through cash on hand, funds generated from opera-

tions, equipment leases and funds available under our credit facilities, we will

consider alternative financing as appropriate for market conditions.

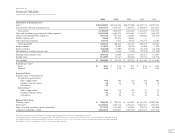

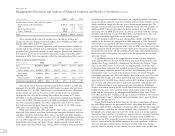

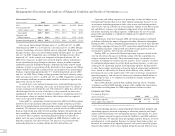

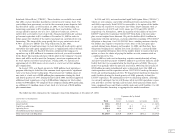

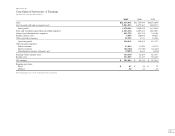

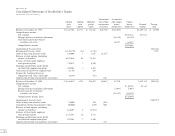

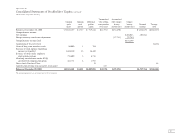

The following table summarizes the Company’s long-term obligations at December 29, 2001:

Payments due by Period

Contractual Cash Obligations Less than After 5

(Dollars in millions) Total 1 year 1–3 years 4–5 years years

Long-term debt $ 555.6 $308.0 $ — $ — $ 247.6

Capital lease obligations 122.9 15.9 25.1 13.2 68.7

Operating leases 2,590.4 400.0 645.8 469.0 1,075.6

Unconditional purchase obligations 2.1 2.1 — — —

Total contractual cash obligations $3,271.0 $726.0 $670.9 $482.2 $1,391.9