Ingram Micro 2001 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2001 Ingram Micro annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

|

|

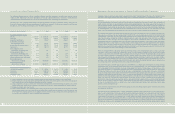

Management’s Discussion and Analysis (continued)

Capital Resources

Our cash and cash equivalents totaled $273.1 million and $150.6 million at December 29, 2001 and December 30, 2000, respectively.

In March 2000, we entered into a revolving five-year accounts receivable securitization program in the U.S., which provides for the

issuance of up to $700 million in commercial paper. In connection with this program most of our U.S. trade accounts receivable are

transferred without recourse to a trust, in exchange for a beneficial interest in the total pool of trade receivables. The trust has issued

fixed-rate, medium-term certificates and has the ability to support a commercial paper program through the issuance of undivided

interests in the pool of trade receivables to third parties. Sales of undivided interests to third parties under this program result in a

reduction of total accounts receivable in our consolidated balance sheet. The excess of the trade accounts receivable transferred over

amounts sold to and held by third parties at any one point in time represents our retained interest in the transferred accounts receivable

(“securitized receivables”) and is shown in our consolidated balance sheet as a separate caption under accounts receivable. Retained

interests are carried at their fair market value, estimated as the net realizable value, which considers the relatively short liquidation

period and includes an estimated provision for credit losses. At December 29, 2001 and December 30, 2000, the amount of undivided

interests sold to and held by third parties under this U.S. program totaled $80.0 million and $700.0 million, respectively.

We also have certain other revolving facilities relating to accounts receivable in Europe and Canada which provide up to approximately

$248 million of additional financing capacity. Under these programs, approximately $142.3 million and $210.2 million of trade accounts

receivable were sold to and held by third parties at December 29, 2001 and December 30, 2000, respectively, resulting in a further reduction

of trade accounts receivable in our consolidated balance sheet.

The aggregate amount of trade accounts receivable sold to and held by third parties under the U.S., Europe and Canada programs, or

off-balance sheet debt, as of December 29, 2001 and December 30, 2000 totaled approximately $222.3 million and $910.2 million,

respectively. This decrease reflects our lower financing needs as a result of our lower volume of business and improvements in working

capital management. The decrease in amounts sold to and held by third parties generally results in an increase in our retained interests

in securitized receivables. We believe that available funding under our accounts receivable financing programs provides us increased

flexibility to make incremental investments in strategic growth initiatives and to manage working capital requirements, and that there

are sufficient trade accounts receivable to support the U.S., European and Canadian accounts receivable financing programs.

As is customary in trade accounts receivable securitization arrangements, credit ratings downgrading the third party issuer of commercial

paper or a back-up liquidity provider (which provides a source of funding if the commercial paper market cannot be accessed) could result

in an adverse change or loss of our financing capacity under these programs if the commercial paper issuer and/or liquidity back-up

provider is not replaced. Loss of such financing capacity could have a material adverse effect on our financial condition and results of

operations. However, based on our assessment of the duration of these programs, the history and strength of the financial partners

involved, other historical data, and the remoteness of such contingencies, we believe it is unlikely that any of these risks will occur.

On August 16, 2001, we sold $200.0 million of 9.875% senior subordinated notes due 2008 at an issue price of 99.382%, resulting in net

cash proceeds of approximately $195.1 million, net of issuance costs of approximately $3.7 million. Under the terms of these notes, we are

required to comply with certain restrictive covenants, including restrictions on the incurrence of additional indebtedness, the amount

of dividends we can pay and the amount of capital stock we can repurchase (see Note 7 to consolidated financial statements for further

discussion on the terms for redemption).

On August 16, 2001, we also entered into interest rate swap agreements with two financial institutions, the effect of which was to swap

our fixed rate obligation on our senior subordinated notes for a floating rate obligation based on 90-day LIBOR plus 4.260%. All other

financial terms of the interest rate swap agreement are identical to those of the senior subordinated notes, except for the quarterly payments

of interest, which will be on November 15, February 15, May 15 and August 15 in each year, commencing on November 15, 2001 and ending

on the termination date of the swap agreement. These interest rate swap arrangements contain ratings conditions requiring more

frequent posting of collateral and at minimum increments if our ratings decline to certain set levels (for example, the ratings condition

is triggered if our S&P ratings decline to “B” or below or our Moody’s ratings decline to “B2” or below). At December 29, 2001, the

marked-to-market value of the interest rate swap amounted to $6.1 million, which is recorded in other assets with an offsetting

adjustment to the hedged debt, bringing the total carrying value of the senior subordinated notes to $204.9 million.

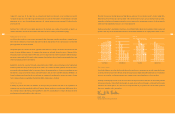

27

Management’s Discussion and Analysis (continued)

Our net sales in the fourth quarter of each fiscal year have generally been higher than those in the other three quarters in the same fiscal

year. However, in 2001, our first quarter sales were higher than our fourth quarter sales because of the sluggish demand for technology

products and services which worsened after the first quarter of 2001. The general trend of higher fourth quarter net sales is attributable

to calendar year-end business purchases and holiday period purchases made by customers.

Liquidity and Capital Resources

Cash Flows

We have financed our growth and cash needs largely through income from operations, borrowings, sales of accounts receivable through

established accounts receivable facilities, trade and supplier credit, the sale of convertible debentures in June 1998 and senior subordinated

notes in August 2001, and the sale of Softbank common stock in December 1999 and January 2000 (see Notes 2 and 8 to consolidated

financial statements).

One of our ongoing objectives is to improve the use of working capital and put assets to work through increasing inventory turns and

steady management of vendor payables and customer receivables. In this regard and in combination with the lower volume of business,

we reduced our overall debt level in 2001, thereby lowering our overall debt-to-capitalization ratio, including off-balance sheet debt

related to our accounts receivable financing programs, to 26.7% at December 29, 2001 compared to 43.7% and 45.0% at December 30,

2000 and January 1, 2000, respectively. Although we have realized significant improvements in working capital management and debt

reduction and we continue to strive for further improvements, no assurance can be made that we will be able to maintain our current

debt levels. The following is a detailed discussion of our cash flows for 2001, 2000 and 1999.

Net cash provided by operating activities was $286.7 million, $839.1 million, and $586.4 million in 2001, 2000 and 1999, respectively.

The significant decrease in cash provided by our operating activities was primarily attributable to the reduction in the amounts sold to

and held by third parties under our accounts receivable programs and the decrease in net income, partially offset by a greater decrease

in other working capital items primarily resulting from our continued focus on managing working capital and the overall lower volume

of business. The increase in cash provided by operating activities in 2000 compared to 1999 was primarily attributable to higher net

income and an increase in the amount of accounts receivable sold to and held by third parties under our accounts receivable facilities,

offset by a decrease in trade creditor financing of product inventory.

Net cash used by investing activities was $70.3 million, $19.5 million, and $138.4 million in 2001, 2000, and 1999, respectively. The net cash

used by investing activities in 2001 was primarily due to capital expenditures of approximately $86.4 million, partially offset by cash

proceeds from the sale of property and equipment of approximately $20.3 million. In 2000, we used approximately $146.1 million in cash

for capital expenditures, which was partially offset by the proceeds from the sale of Softbank common stock totaling approximately $119.2

million. In 1999, we used approximately $241.9 million in cash for acquisitions, net of cash acquired, and $135.3 million for capital

expenditures, which were partially offset by the proceeds from the sale of Softbank common stock totaling approximately $230.1 million.

Net cash used by financing activities was $78.3 million, $805.3 million, and $427.3 million in 2001, 2000, and 1999, respectively. Net cash

used by financing activities in 2001 primarily resulted from the repurchase of convertible debentures for $225.0 million and net repayments

of our revolving credit and other debt facilities. This was primarily enabled through cash provided by operations, continued focus on

working capital management and the reduction in net revenues, as well as by the proceeds from our issuance of senior subordinated

notes of $195.1 million. Net cash used by financing activities in 2000 was primarily due to the repurchase of the convertible debentures

of $231.3 million and the net repayment of borrowings under the revolving credit facilities and other debt facilities through the use of

cash provided by operations and the continued focus on working capital management, as well as the proceeds received from the sale of

Softbank common stock in 2000. Net cash used by financing activities in 1999 was primarily due to the repurchase of the convertible

debentures of $50.3 million and the net repayment of borrowings under the revolving credit facilities through the use of the proceeds

received from the sale of Softbank common stock in 1999, as well as the continued focus on working capital management.

Acquisitions

In December 2001, we concluded a business combination involving certain assets and liabilities of our former subdistributor in the People’s

Republic of China, which was accounted for in accordance with FAS 141. In addition, during September 2001, we acquired certain assets of an

IT distribution business in the United Kingdom. The purchase price for these transactions aggregated $15.9 million in cash and was

allocated to the assets acquired and liabilities assumed based on their estimated fair values on the transaction dates, resulting in the

recording of approximately $105.4 million of goodwill. These transactions had no significant impact on our consolidated results of operations.

26