Carphone Warehouse 2007 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2007 Carphone Warehouse annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

2007Performance UpdateOur Strategy

The Carphone Warehouse Group PLC Annual Report 2007

8

OUR VIRTUOUS CIRCLE OF PERFORMANCE

Investment

Our long-term approach to investment creates sustainable competitive

advantage in our chosen markets. Investment is not just about

capex – although our commitment to store openings and exchange

unbundling is significant – it is also about marketing, brand-building

and customer recruitment.

Scale

We aim to be a mass market provider in our major business lines by

driving for volume ahead of margin. We then use our increased

presence in the market to improve our supplier terms and reinvest

these benefits in the customer proposition.

Efficiency

Scale also creates significant efficiencies for our business, through

leveraging our fixed cost store base and telecoms infrastructure. We

seek to maintain our competitive advantage by continued investment

across the business.

Proposition

We are absolutely committed to delivering value to customers across

all our services. Investment in the right platforms is key to our ability to

develop a compelling customer proposition, as it allows us to build

scale, and offer greater value and an improved customer experience.

I

N

V

E

S

T

M

E

N

T

S

C

A

L

E

P

R

O

P

O

S

I

T

I

O

N

E

F

F

I

C

I

E

N

C

Y

OUR OPERATIONS WHAT WE SAID WE’D DO IN 2006/07

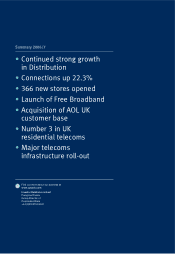

Retail and Online • Open a further 250 new stores

• Differentiate proposition through

handset range

• Continue to drive growth in

subscription connections

• Continue to explore non-UK

Online opportunities

Insurance • Further base growth

• Improve penetration with

new products

Ongoing • Revenue growth of 15-20%

Distribution division

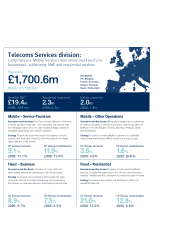

OUR OPERATIONS WHAT WE SAID WE’D DO IN 2006/07

Mobile –

Service Provision

• Further growth in

subscription base

• Stabilisation of ARPU trend

through focus on higher

quality channels

Mobile –

Other Operations

• Launch Mobile World in

other markets

• Refine Fresh proposition

to maximise customer

lifetime values

• Build towards target of 1m

Virgin Mobile customers

within 3 years

Fixed –

Business

• Focus on local loop unbundling

programme to hit target of

1,000 exchanges by May 2007

• Leverage LLU platform to build

corporate broadband products

• Build on initial TalkTalk

Business success

Fixed –

Residential

• Focus on rapid recruitment of

broadband customers

• Manage the successful

migration of customers onto

unbundled lines

• Complete integration of

Onetel acquisition

• Raise line rental penetration on

voice customer base to 60%

Telecoms Services division