Vonage 2010 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2010 Vonage annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

|

|

ITEM

7.

M

anagement’s Discussion and Analysis o

f

Financia

l

Condition and Results of Operation

s

You should read the following discussion together wit

h

“

S

elected Financial Data” and our consolidated financial state

-

m

ents an

d

t

h

ere

l

ate

d

notes

i

nc

l

u

d

e

d

e

l

sew

h

ere

i

nt

hi

s

A

nnua

l

R

eport on Form 10-K. This discussion contains forward-lookin

g

statements

,

which involve risks and uncertainties.

O

ur actual

r

esults may differ materially from those we currently anticipate as

a

result of many factors, including the factors we describe under

“I

tem 1

A

—

Ri

s

kF

actors,

”

an

d

e

l

sew

h

ere

i

nt

hi

s

A

nnua

lR

eport on

F

orm 10-

K.

OVERVIEW

We are a leadin

g

provider o

f

low-cost communications serv-

i

ces connectin

g

people throu

g

h broadband devices worldwide

.

We rely heavily on our network, which is a flexible, scalable Ses

-

s

ion Initiation Protocol

(

SIP

)

based Voice over Internet Protocol,

or VoIP, network that rides on to

p

o

f

the Internet. This

p

lat

f

orm

enables a user via a sin

g

le “identity,” either a number or use

r

name, to access and utilize services and

f

eatures re

g

ardless o

f

how they are connected to the Internet, includin

g

over 3G, 4G

,

C

able, or DSL broadband networks. This technolo

g

y enables us

t

oo

ff

er attractivel

y

priced services that provide our customers

with access to Vonage voice, messaging, and

f

eatures, regard

-

l

ess o

f

location

,

device

,

or their

f

orm o

f

Internet access

.

O

ur customers include both domestic and internationa

l

l

ong distance callers, which we classi

f

y as customers who that

make 20 or more minutes o

f

international long distance calls pe

r

month within their plan.

O

ur primary product offering is Vonag

e

W

or

ld

, a res

id

ent

i

a

l

p

l

an w

i

t

h

un

li

m

i

te

d

ca

lli

ng

d

omest

i

ca

ll

yan

d

t

o more than 60 countries, including India, Mexico, and

C

hina

,

for a flat monthl

y

rate

.

W

e introduced our first mobile offering in late 2009, an

outbound long distance calling application, and Vonage Mobil

e

for Facebook in Au

g

ust 2010, enablin

g

inbound and outbound

callin

g

to a user’s Facebook friends. We anticipate levera

g

in

g

our technolo

g

y to offer additional applications for mobile and

other connected devices to address lar

g

e existin

g

markets

.

I

n December 2010, we completed the re

f

inancing o

f

our out

-

s

tanding notes payable. The terms of the new loan include sig

-

n

ificantl

y

lower interest rates and less restrictive covenants than the

prior debt. We believe this refinancing helps to de-risk the busines

s

by simplifying the complex covenant structure and it gives u

s

g

reater flexibility to deploy the cash generated by our business.

We serviced approximatel

y

2.4 million subscriber lines as of

December 31, 2010.

S

ubscribers can sign-up through our direc

t

s

ales channel, as represented b

y

web-sites and toll free num

-

b

ers, or purc

h

ase

d

ev

i

ces at our reg

i

ona

l

an

d

nat

i

ona

l

reta

il

ers,

i

ncluding Walmart and Fry’s Electronics.

O

ur primary source o

f

r

evenue is subscription fees that we charge customers for our

s

erv

i

ce p

l

ans, pr

i

mar

il

y on a mont

hl

y

b

as

i

s.

W

ea

l

so generat

e

r

evenue from call usage that is not included in customers’ serv

-

i

ce plans and for additional features that customers add to their

s

ervice plans. We bill customers in the United

S

tates,

C

anada,

and the United Kingdom.

C

ustomers in the United

S

tates repre

-

s

ented 94% of our subscriber lines at December 31

,

2010.

T

rends in Our Industry and Key Operating Data A number o

f

trends in our industry have a si

g

ni

f

icant e

ff

ect on our results o

f

operations and are important to an understandin

g

o

f

our

f

inancial statements. The table below includes key operatin

g

data that ou

r

mana

g

ement uses to measure the

g

rowth and operatin

g

per

f

ormance o

f

our business

:

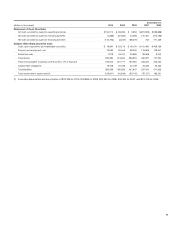

F

or t

h

e

Y

ears

E

n

d

e

dD

ecem

b

er

3

1

,

2

0

1

0

2

009

2

008

G

ross subscriber line additions

640

,

20

57

48

,

681 9

5

2

,

014

C

han

g

e in net subscriber line

s

(

30,013

)(

155,458

)

26,92

9

S

ubscriber lines

(

at

p

eriod end

)

2

,

404

,

883 2

,

434

,

896 2

,

60

7,

1

5

6

A

vera

g

e monthly customer churn 2.4

%

3.1

%

3.1

%

A

vera

g

e monthly revenue per lin

e

$

30.48

$

29.49

$

28.9

2

A

vera

g

e monthly telephony services revenue per line

$

30.06

$

28.68

$

27.82

A

vera

g

e monthly direct cost of telephony services per line

$

8.40

$

7.08

$

7.27

Marketin

g

costs per

g

ross subscriber line addition

$

309.54

$

304.52

$

266.1

4

Employees

(

excludin

g

temporary help

)(

at period end

)

1,140 1,225 1,491

B

roa

db

an

d

a

d

opt

i

on

.

The number of United

S

tates house

-

holds with broadband Internet access has grown significantly.

O

n March 16

,

2010

,

the Federal

C

ommunications

C

ommissio

n

(

“F

CC

”

)

released its National Broadband Plan, which seeks

,

th

roug

h

support

i

ng

b

roa

db

an

dd

ep

l

oyment an

d

programs, t

o

encourage broadband adoption for the approximatel

y

1

00 million United

S

tates residents who do not have broadban

d

at home. We expect the trend of greater broadband adoption to

continue. We benefit from this trend because our servic

e

r

equ

i

res a

b

roa

db

an

dI

nternet connect

i

on an

d

our potent

i

a

l

a

dd

ressa

bl

e mar

k

et

i

ncreases as

b

roa

db

an

d

a

d

opt

i

o

n

i

ncreases.

C

ompetitive landscape

.

W

e face intense competition from

t

ra

di

t

i

ona

l

te

l

ep

h

one compan

i

es, w

i

re

l

ess compan

i

es, ca

bl

e

compan

i

es, an

d

a

l

ternat

i

ve vo

i

ce commun

i

cat

i

on prov

id

ers

.

2

6

VO

NA

G

E ANN

U

AL REP

O

RT 2010