United Healthcare 2011 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2011 United Healthcare annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

62

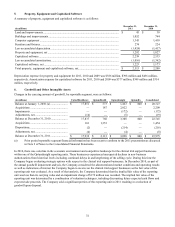

Intangible assets

Finite-lived, separately-identifiable intangible assets are acquired in business combinations and are assets that represent future

expected benefits but lack physical substance (e.g., membership lists, customer contracts, trademarks and technology). The

Company does not have material holdings of indefinite lived intangible assets. The Company's intangible assets are initially

recorded at their fair values and are then amortized over their expected useful lives.

The Company's intangible assets are subject to impairment tests when events or circumstances indicate that a finite-lived

intangible asset's (or asset group's) carrying value may exceed its estimated fair value. Consideration is given to a number of

potential impairment indicators. Following the identification of any potential impairment indicators, to determine whether an

impairment exists, the Company would calculate the estimated fair value of a finite-lived intangible asset using the

undiscounted cash flows that are expected to result from the use of the asset or related group of assets. Once it is determined

that an impairment exists, the amount by which the carrying value exceeds the estimated fair value is recorded as an

impairment.

There were no material impairments of finite-lived intangible assets during the year ended December 31, 2011.

Other Policy Liabilities

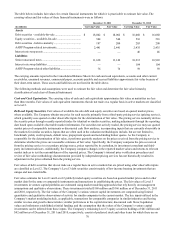

Other policy liabilities include the RSF associated with the AARP Program (described below), health savings account deposits,

deposits under the Medicare Part D program (see “Medicare Part D Pharmacy Benefits” above), accruals for premium rebate

payments under the Health Reform Legislation, the current portion of future policy benefits and customer balances. Customer

balances represent excess customer payments and deposit accounts under experience-rated contracts. At the customer's option,

these balances may be refunded or used to pay future premiums or claims under eligible contracts.

Underwriting gains or losses related to the AARP Program are directly recorded as an increase or decrease to the RSF and

accrue to the overall benefit of the AARP policyholders, unless cumulative net losses were to exceed the balance in the RSF.

The primary components of the underwriting results are premium revenue, medical costs, investment income, administrative

expenses, member service expenses, marketing expenses and premium taxes. To the extent underwriting losses exceed the

balance in the RSF, losses would be borne by the Company. Deficits may be recovered by underwriting gains in future periods

of the contract. To date, the Company has not been required to fund any underwriting deficits. Changes in the RSF are reported

in Medical Costs in the Consolidated Statement of Operations. As of December 31, 2011 and 2010, the balance in the RSF was

$1.3 billion. The Company believes the RSF balance as of December 31, 2011 is sufficient to cover potential future

underwriting and other risks and liabilities associated with the contract.

Income Taxes

Deferred income tax assets and liabilities are recognized for the differences between the financial and income tax reporting

bases of assets and liabilities based on enacted tax rates and laws. The deferred income tax provision or benefit generally

reflects the net change in deferred income tax assets and liabilities during the year, excluding any deferred income tax assets

and liabilities of acquired businesses. The current income tax provision reflects the tax consequences of revenues and expenses

currently taxable or deductible on various income tax returns for the year reported.

Future Policy Benefits and Reinsurance Receivable

Future policy benefits represent account balances that accrue to the benefit of the policyholders, excluding surrender charges,

for universal life and investment annuity products and for long-duration health policies sold to individuals for which some of

the premium received in the earlier years is intended to pay benefits to be incurred in future years. As a result of the 2005 sale

of the life and annuity business within the Company's Golden Rule Financial Corporation subsidiary under an indemnity

reinsurance arrangement, the Company has maintained a liability associated with the reinsured contracts, as it remains

primarily liable to the policyholders, and has recorded a corresponding reinsurance receivable due from the purchaser. As of

December 31, 2011, the Company had an aggregate $1.9 billion reinsurance receivable, of which $125 million was recorded in

Other Current Receivables and $1.8 billion was recorded in Other Assets in the Consolidated Balance Sheets. As of

December 31, 2010, the Company had an aggregate $2.0 billion reinsurance receivable, of which $126 million was recorded in

Other Current Receivables and $1.9 billion was recorded in Other Assets in the Consolidated Balance Sheets. The Company

evaluates the financial condition of the reinsurer and only records the reinsurance receivable to the extent of probable recovery.

Currently, the reinsurer is rated by A.M. Best as “A+.”

Policy Acquisition Costs

The Company's short duration health insurance contracts typically have a one-year term and may be cancelled by the customer

with at least 30 days notice. Costs related to the acquisition and renewal of short duration customer contracts are charged to