United Healthcare 2011 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2011 United Healthcare annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

30

UnitedHealthcare serves the health benefits needs of individuals across life's stages through three businesses. UnitedHealthcare

Employer & Individual serves individual consumers and employers. The unique health needs of seniors are served by

UnitedHealthcare Medicare & Retirement. UnitedHealthcare Community & State serves the public health marketplace, offering

states innovative Medicaid solutions.

Optum serves health system participants including consumers, physicians, hospitals, governments, insurers, distributors and

pharmaceutical companies, through its OptumHealth, OptumInsight and OptumRx businesses.

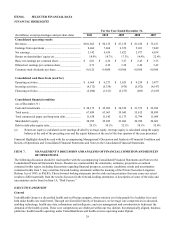

Revenues

Our revenues are primarily comprised of premiums derived from risk-based health insurance arrangements in which the

premium is typically at a fixed rate per individual served for a one-year period, and we assume the economic risk of funding

our customers’ health care benefits and related administrative costs. Effective in 2011, commercial health plans with medical

loss ratios on fully insured products, as calculated under the definitions in the Health Reform Legislation and implementing

regulations, that fall below certain targets (85% for large employer groups, 80% for small employer groups and 80% for

individuals, subject to state-specific exceptions) are required to rebate ratable portions of their premiums annually. As a result,

our quarterly premium revenue may be reduced by a pro rata estimate of our full-year premium rebate payable under the Health

Reform Legislation. Any required rebate payments for the current year are made in the third quarter of the subsequent year. We

also generate revenues from fee-based services performed for customers that self-insure the health care costs of their employees

and employees’ dependants. For both risk-based and fee-based health care benefit arrangements, we provide coordination and

facilitation of medical services; transaction processing; health care professional services; and access to contracted networks of

physicians, hospitals and other health care professionals. We also generate service revenues from our Optum businesses.

Product revenues are mainly comprised of products sold by our pharmacy benefit management business. We derive investment

income primarily from interest earned on our investments in debt securities; investment income also includes gains or losses

when investment securities are sold, or other-than-temporarily impaired.

Operating Costs

Medical Costs. Our operating results depend in large part on our ability to effectively estimate, price for and manage our

medical costs through underwriting criteria, product design, negotiation of favorable care provider contracts and care

coordination programs. Controlling medical costs requires a comprehensive and integrated approach to organize and advance

the full range of interrelationships among patients/consumers, health professionals, hospitals, pharmaceutical/technology

manufacturers and other key stakeholders.

Medical costs include estimates of our obligations for medical care services rendered on behalf of insured consumers for which

we have not yet received or processed claims, and our estimates for physician, hospital and other medical cost disputes. In

every reporting period, our operating results include the effects of more completely developed medical costs payable estimates

associated with previously reported periods.

Our medical care ratio, calculated as medical costs as a percentage of premium revenues, reflects the combination of pricing,

rebates, benefit designs, consumer health care utilization and comprehensive care facilitation efforts.

Operating Costs. Operating costs are primarily comprised of costs related to employee compensation and benefits, agent and

broker commissions, premium taxes and assessments, professional fees, advertising and occupancy costs. We seek to improve

our operating cost ratio, calculated as operating costs as a percentage of total revenues, for an equivalent mix of business.

However, changes in business mix, such as increases in the size of our health services businesses may impact our operating

costs and operating cost ratio.

Cash Flows

We generate cash primarily from premiums, service and product revenues and investment income, as well as proceeds from the

sale or maturity of our investments. Our primary uses of cash are for payments of medical claims and operating costs, payments

on debt, purchases of investments, acquisitions, dividends to shareholders and common stock repurchases. For more

information on our cash flows, see “Liquidity” below.

Business Trends

Our businesses participate in the U.S. health economy, which comprises approximately 18% of U.S. gross domestic product

and has grown consistently for many years. We expect overall spending on health care in the U.S. to continue to grow in the

future, due to inflation, medical technology and pharmaceutical advancement, regulatory requirements, demographic trends in

the U.S. population and national interest in health and well-being. The rate of market growth may be affected by a variety of

factors, including macro-economic conditions and enacted health care reforms, which could also impact our results of