Red Lobster 2011 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2011 Red Lobster annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

|

|

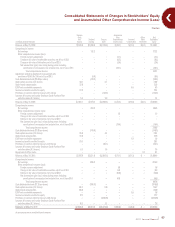

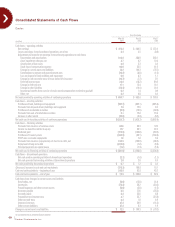

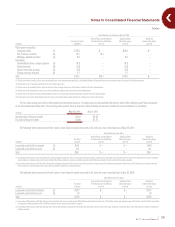

Notes to Consolidated Financial Statements

Darden

›

2011 Annual Report 55

NOTE 8

OTHER CURRENT LIABILITIES

The components of other current liabilities are as follows:

(in millions)

May 29, 2011 May 30, 2010

Non-qualified deferred compensation plan $200.1 $158.1

Sales and other taxes 6 1. 5 51.5

Insurance-related 33.6 30.4

Employee benefits 33.8 32.9

Derivative liabilities 23.2 12.1

Accrued interest 14.0 17.7

Miscellaneous 43.1 38.2

Total other current liabilities $409.3 $340.9

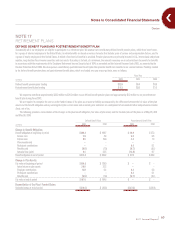

NOTE 9

LONG-TERM DEBT

The components of long-term debt are as follows:

(in millions)

May 29, 2011 May 30, 2010

4.875% senior notes due August 2010 $ — $ 150.0

7.450% medium-term notes due April 2011 — 75.0

5.625% senior notes due October 2012 350.0 350.0

7.125% debentures due February 2016 100.0 100.0

6.200% senior notes due October 2017 500.0 500.0

6.000% senior notes due August 2035 150.0 150.0

6.800% senior notes due October 2037 300.0 300.0

ESOP loan with variable rate of interest

(0.55% at May 29, 2011) due December 2018 8.0 9.8

Total long-term debt 1,408.0 1,634.8

Fair value hedge 3.7 3.8

Less issuance discount (4.4) (4.9)

Total long-term debt less issuance discount 1,407.3 1,633.7

Less current portion — (225.0)

Long-term debt, excluding current portion $1,407.3 $1,408.7

We maintain a $750.0 million revolving credit facility under a Credit Agreement

(Revolving Credit Agreement) dated September 20, 2007 with Bank of America,

N.A. (BOA), as administrative agent, and the lenders (Revolving Credit Lenders)

and other agents party thereto. The Revolving Credit Agreement is a senior

unsecured debt obligation of the Company and contains customary representations,

affirmative and negative covenants (including limitations on liens and subsidiary

debt, and a maximum consolidated lease adjusted total debt to total capitalization

ratio of 0.75 to 1.00) and events of default usual for credit facilities of this type.

As of May 29, 2011, we were in compliance with all covenants under the Revolving

Credit Agreement.

The Revolving Credit Agreement matures on September 20, 2012, and the

proceeds may be used for commercial paper back-up, working capital and capital

expenditures, the refinancing of certain indebtedness as well as general corporate

purposes. The Revolving Credit Agreement also contains a sub-limit of $150.0

million for the issuance of letters of credit. The borrowings and letters of credit

obtained under the Revolving Credit Agreement may be denominated in U.S. Dollars,

Euro, Sterling, Yen, Canadian Dollars and each other currency approved by the

Revolving Credit Lenders. The Company may elect to increase the commitments

under the Revolving Credit Agreement by up to $250.0 million (to an aggregate

amount of up to $1.0 billion), subject to the Company obtaining commitments

from new and existing lenders for the additional amounts.

Loans under the Revolving Credit Agreement bear interest at a rate of LIBOR

plus a margin determined by reference to a ratings-based pricing grid, or the base

rate (which is defined as the higher of the BOA prime rate and the Federal Funds

rate plus 0.500 percent). Assuming a “BBB” equivalent credit rating level, the

applicable margin under the Revolving Credit Agreement will be 0.350 percent. We

may also request that loans under the Revolving Credit Agreement be made at

interest rates offered by one or more of the Revolving Credit Lenders, which may

vary from the LIBOR or base rate, for up to $100.0 million of borrowings. The

Revolving Credit Agreement requires that we pay a facility fee on the total amount

of the facility (ranging from 0.070 percent to 0.175 percent, based on our credit

ratings) and, in the event that the outstanding amounts under the Revolving Credit

Agreement exceeds 50 percent of the aggregate commitments under the Revolving

Credit Agreement, a utilization fee on the total amount outstanding under the

facility (ranging from 0.050 percent to 0.150 percent, based on our credit ratings).

As of May 29, 2011, we had no outstanding balances under the Revolving Credit

Agreement. As of May 29, 2011, $185.5 million of commercial paper and $68.2 million

of letters of credit were outstanding, which are backed by this facility. After

consideration of borrowings currently outstanding and commercial paper and letters

of credit backed by the Revolving Credit Agreement, as of May 29, 2011, we had

$496.3 million of credit available under the Revolving Credit Agreement.

The interest rates on our $350.0 million of unsecured 5.625 percent senior

notes due October 2012, $500.0 million of unsecured 6.200 percent senior notes

due October 2017 and $300.0 million of unsecured 6.800 percent senior notes

due October 2037 (collectively, the New Senior Notes) is subject to adjustment

from time to time if the debt rating assigned to the series of the New Senior

Notes is downgraded below a certain rating level (or subsequently upgraded).

The maximum adjustment is 2.000 percent above the initial interest rate and the

interest rate cannot be reduced below the initial interest rate. As of May 29, 2011,

no adjustments to these interest rates had been made. We may redeem any

series of the New Senior Notes at any time in whole or from time to time in part,

at the principal amount plus a make-whole premium. If we experience a change

of control triggering event, we may be required to purchase the New Senior

Notes from the holders.

All of our long-term debt currently outstanding is expected to be repaid

entirely at maturity with interest being paid semi-annually over the life of the

debt. The aggregate maturities of long-term debt for each of the five fiscal years

subsequent to May 29, 2011, and thereafter are as follows:

Fiscal Year Amount

2012 $ —

2013 350.0

2014 —

2015 —

2016 100.0

Thereafter 958.0

Long-term debt $1,408.0