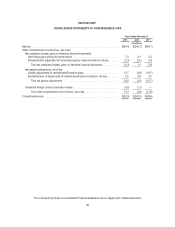

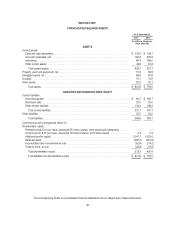

Memorex 2013 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2013 Memorex annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

|

|

the tax benefit is measured and recognized as the largest amount of tax benefit that, in our judgment, is greater than

50 percent likely to be realized.

The total amount of unrecognized tax benefits as of December 31, 2013 was $5.3 million, excluding accrued interest

and penalties described below. If the unrecognized tax benefits were recognized in our Consolidated Financial Statements,

$5.3 million would affect income tax expense and our related effective tax rate.

Interest and penalties recorded for uncertain tax positions are included in our income tax provision. As of December 31,

2013, $1.1 million of interest and penalties was accrued, excluding the tax benefit of deductible interest. The reversal of

accrued interest and penalties would affect income tax expense and our related effective tax rate.

Our U.S. federal income tax returns for 2010 through 2012 are subject to examination by the Internal Revenue Service.

With few exceptions, we are no longer subject to examination by foreign tax jurisdictions, or state and city tax jurisdictions for

years before 2006. In the event that we have determined not to file tax returns with a particular state or city, all years remain

subject to examination by the tax jurisdiction.

The ultimate outcome of tax matters may differ from our estimates and assumptions. Unfavorable settlement of any

particular issue may require the use of cash and could result in increased income tax expense. Favorable resolution could

result in reduced income tax expense. It is reasonably possible that our unrecognized tax benefits could increase or decrease

significantly during the next twelve months due to the resolution of certain U.S. and international tax uncertainties; however it

is not possible to estimate the potential change at this time.

Intangibles. We record all assets and liabilities acquired in purchase acquisitions, including intangibles, at estimated

fair value. Intangible assets with a definite life are amortized based on a pattern in which the economic benefits of the assets

are consumed, typically with useful lives ranging from one to 30 years. The initial recognition of intangible assets, the

determination of useful lives and, if necessary, subsequent impairment analysis require management to make subjective

judgments concerning estimates of how the acquired assets will perform in the future using certain valuation methods

including discounted cash flow analysis. We evaluate assets on our balance sheet, including such intangible assets,

whenever events or changes in circumstances indicate that their carrying value may not be recoverable. Factors such as

unfavorable variances from forecasted cash flows, established business plans or volatility inherent to external markets and

industries may indicate a possible impairment that would require an impairment test. While we believe that the current

carrying value of these assets is not impaired, materially different assumptions regarding future performance of our

businesses, which in many cases require subjective judgments concerning estimates, could result in significant impairment

losses. The test for impairment requires a comparison of the carrying value of the asset or asset group with their estimated

undiscounted future cash flows. If the carrying value of the asset or asset group is considered impaired, an impairment charge

is recorded for the amount by which the carrying value of the asset or asset group exceeds its fair value. See Note 6 —

Intangible Assets and Goodwill for information on our 2013 and 2012 intangible assets.

Goodwill. We record all assets and liabilities acquired in purchase acquisitions, including goodwill, at fair value. The

initial recognition of goodwill and subsequent impairment analysis require management to make subjective judgments

concerning estimates of how the acquired assets will perform in the future using valuation methods including discounted cash

flow analysis. Goodwill is the excess of the cost of an acquired entity over the amounts assigned to assets acquired and

liabilities assumed in a business combination. Goodwill is not amortized. We test the carrying amount of a reporting unit’s

goodwill for impairment on an annual basis during the fourth quarter of each year (as of November 30) or if an event occurs or

circumstances change that would warrant impairment testing during an interim period.

Goodwill is considered impaired when its carrying amount exceeds its implied fair value. The first step of the impairment

test involves comparing the fair value of the reporting unit to which goodwill was assigned to its carrying amount. The second

step of the impairment test compares the implied fair value of the reporting unit’s goodwill with the carrying amount of the

reporting unit’s goodwill. If the carrying amount of the reporting unit’s goodwill is greater than the implied fair value of the

reporting unit’s goodwill an impairment loss must be recognized for the excess. This involves measuring the fair value of the

reporting unit’s assets and liabilities (both recognized and unrecognized) at the time of the impairment test. The difference

41