Hyundai 2015 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2015 Hyundai annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

HYUNDAI MOTOR COMPANY Annual Report 2015

110 111

recognized for all deductible temporary differences to the

extent that it is probable that taxable profits will be available

against which those deductible temporary differences can be

utilized. Such deferred tax assets and liabilities shall not be

recognized if the temporary difference arises from goodwill

or from the initial recognition (other than in a business com-

bination) of other assets and liabilities in a transaction that

affects neither the taxable profit nor the accounting profit.

Deferred tax liabilities are recognized for taxable tempo-

rary differences associated with investments in subsidiaries

and associates, and interests in joint ventures, except when

the Group is able to control the timing of the reversal of the

temporary difference and it is probable that the temporary

difference will not reverse in the foreseeable future. Deferred

tax assets arising from deductible temporary differences as-

sociated with such investments and interests are only recog-

nized to the extent that taxable profit will be available against

which the temporary difference can be utilized and they are

expected to be reversed in the foreseeable future.

The carrying amount of deferred tax assets is reviewed at the

end of each reporting period and reduced to the extent that

it is no longer probable that sufficient taxable profits will be

available to allow all or part of the asset to be recovered.

Deferred tax assets and liabilities are measured at the tax

rates that are expected to be applied in the period in which

the liability is settled or the asset is realized, based on tax

rates and tax laws that have been enacted or substantively

enacted by the end of the reporting period. The measurement

of deferred tax assets and liabilities reflects the tax con-

sequences that would follow from the manner in which the

Group expects to recover or settle the carrying amount of its

assets and liabilities at the end of the reporting period.

Deferred tax assets and liabilities are offset when there is a

legally enforceable right to offset current tax assets against

current tax liabilities and when they relate to income tax lev-

ied by the same taxation authority. Also, they are offset when

different taxable entities which intend either to settle current

tax liabilities and assets on a net basis, or to realize the assets

and settle the liabilities simultaneously, in each future period

in which significant amounts of deferred tax liabilities or as-

sets are expected to be settled or recovered.

3) Current and deferred tax for the year

Current and deferred tax are recognized in profit or loss, ex-

cept when they relate to items that are recognized in other

comprehensive income or directly in equity, or items arising

from initial accounting treatments of a business combination.

The tax effect arising from a business combination is included

in the accounting for the business combination.

(22) Treasury stock

When the Group repurchases its equity instruments (treasury

stock), the incremental costs and net of tax effect are de-

ducted from equity and recognized as other capital item de-

ducted from the total equity in the consolidated statements of

financial position. In addition, profits or losses from purchase,

sale or retirement of treasury stocks are directly recognized

in equity and not in current profit or loss.

(23) Financial liabilities and equity instruments

Debt instruments and equity instruments issued by the Group

are recognized as financial liabilities or equity depending on

the contract and the definitions of financial liability and equity

instrument.

1) Equity instruments

An equity instrument is any contract that evidences a residual

interest in the assets of an entity after deducting all of its lia-

bilities. Equity instruments issued by the Group are recognized

at issuance amount net of direct issuance costs.

2) Financial guarantee liabilities

A financial guarantee contract is a contract that requires the

issuer to make specified payments to reimburse the holder

for a loss it incurs because a specified debtor fails to make

payment when due in accordance with the original or modified

terms of a debt instrument.

Financial guarantee contract liabilities are initially measured at

their fair values and, if not designated as at FVTPL, are sub-

sequently measured at the higher of:

● the amount of the obligation under the contract, as deter-

mined in accordance with K-IFRS 1037

Provisions, Contin-

gent Liabilities and Contingent Assets

; and

● the amount initially recognized less, cumulative amortization

recognized in accordance with the K-IFRS 1018

Revenue

3) Financial liabilities at FVTPL

Financial instruments classified as financial liabilities at FVTPL

include contingent consideration that may be paid by an ac-

quirer as part of a business combination to which K-IFRS 1103

applies or financial liability classified as held for trading or

designated as FVTPL upon initial recognition. FVTPL is stated

at fair value and the gains and losses arising on remeasure-

ment and the interest expenses paid in financial liabilities are

recognized in profit and loss.

4) Other financial liabilities

Other financial liabilities are initially measured at fair value,

net of transaction costs. Other financial liabilities are sub-

sequently measured at amortized cost using the effective

interest method, with interest expense recognized on an ef-

fective-yield basis.

5) Derecognition of financial liabilities

The Group derecognizes financial liabilities only when the

Group’s obligations are discharged, cancelled or they expire.

(24) Derivative financial instruments

Derivatives are initially recognized at fair value at the date

the derivative contracts are entered into and are subsequently

remeasured to their fair value at the end of each reporting

period. The resulting gain or loss is recognized in profit or

loss immediately unless the derivative is designated and ef-

fective as a hedging instrument, in such case the timing of

the recognition in profit or loss depends on the nature of the

hedge relationship.

The Group designates certain derivatives as hedging instru-

ments to hedge the risk of changes in fair value of a recog-

nized asset or liability or an unrecognized firm commitment

(fair value hedges) and the risk of changes in cash flow of a

highly probable forecast transaction and the risk of changes

in foreign currency exchange rates of firm commitment (cash

flow hedges).

1) Fair value hedges

The Group recognizes the changes in the fair value of deriv-

atives that are designated and qualified as fair value hedges

are recognized in profit or loss immediately, together with any

changes in the fair value of the hedged asset or liability that

are attributable to the hedged risk. Hedge accounting is dis-

continued when the Group revokes the hedging relationship,

when the hedging instrument expires or is sold, terminated,

or exercised, or when it is no longer qualified for hedge ac-

counting. The fair value adjustment to the carrying amount of

the hedged item arising from the hedged risk is amortized to

profit or loss from that date.

2) Cash flow hedges

The effective portion of changes in the fair value of deriva-

tives that are designated and qualified as cash flow hedges is

recognized in other comprehensive income. The gain or loss

relating to the ineffective portion is recognized immediately in

profit or loss. Amounts previously recognized in other com-

prehensive income and accumulated in equity are reclassified

to profit or loss in the periods when the hedged item affects

profit or loss.

If the forecast transaction results in the recognition of a

non-financial asset or liability, the related gain and loss rec-

ognized in other comprehensive income and accumulated in

equity is transferred from equity to the initial cost of related

non-financial asset or liability.

Cash flow hedge accounting is discontinued when the Group

revokes the hedging relationship, when the hedging instru-

ment expires or is sold, terminated or exercised, or it no

longer qualifies for the criteria of hedging. Any gain or loss

accumulated in equity at that time remains in equity and is

recognized as profit or loss when the forecast transaction

occurs. When the forecast transaction is no longer expected

to occur, the gain or loss accumulated in equity is recognized

immediately in profit or loss.

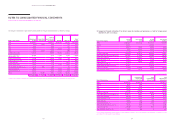

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

AS OF AND FOR THE YEARS ENDED DECEMBER 31, 2015 AND 2014